Fertilizer Shocks Ahead Could Risk Food Supply

The effects of the Middle East conflict on ammonia and urea markets are expected to be global and far-reaching.

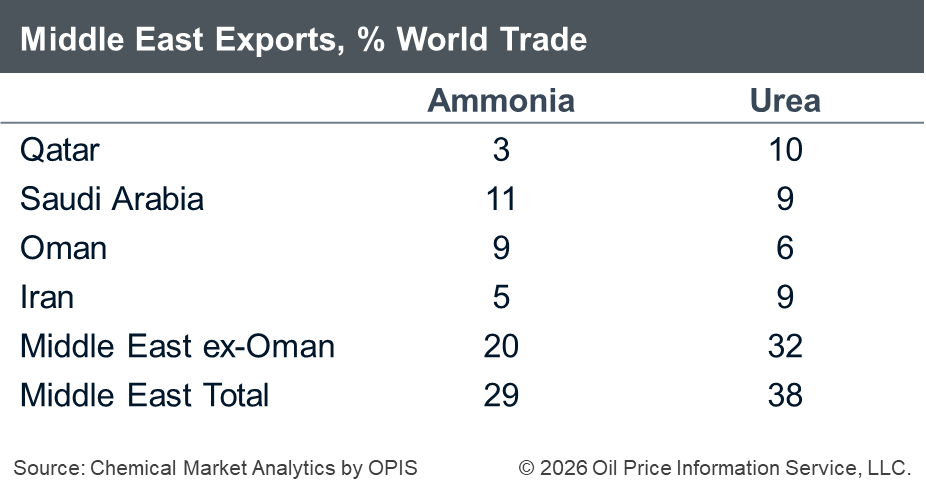

Supply via the Strait of Hormuz accounts for approximately 30-35% of global seaborne urea trade and around 30% of ammonia trade. Outside of Oman, all ammonia and urea exports from the Middle East (including Iran) flow through the strait. Oman has also been affected by the conflict, sustaining attacks on its infrastructure. However, production and exports remain at pre-conflict levels.

The bulk of ammonia produced globally is captive and vertically integrated with downstream urea output. Urea, a major fertilizer, accounts for nearly 60% of global ammonia demand.

At the start of the conflict, Iran shut down ammonia and urea output, while Israel halted gas production at key facilities and suspended exports, which is of particular concern to Egyptian ammonia and urea producers. Iran restarted ammonia and urea production shortly after, and Israel restarted gas production last week. However, the situation remains precarious and the outlook is uncertain, with market participants closely monitoring wider developments.

QatarEnergy also announced the shutdown of its urea (and likely ammonia) output, along with its liquified natural gas (LNG) production, within days of the start of the conflict.

Egyptian and European production is uninterrupted despite feedstock gas concerns. In contrast, India has limited flexibility, as ammonia, urea, and gas imports have been negatively impacted.

The conflict in the Middle East has already had, and will continue to have, a major impact on global ammonia and urea markets. Prices increased by 20-30% within the first two weeks of the conflict and have since increased by well over 50% in most cases.

Ammonia and urea prices are currently near the 2022 peaks and demand destruction is inevitable. In alignment with historical trends, importers, primarily in Europe, have attempted to resist these sharp price increases. However, amid significantly tighter global supply, buyers will have few options but to eventually accept higher prices.

Regarding food production, crop yields are expected to decline amid reduced fertilizer application. However, the global impact will likely be uneven, and countries that are major net importers and rely on imported LNG for domestic ammonia and urea production (such as India) are expected to be the most affected.

–Michael Samueli, Director, Ammonia-Urea, Chemical Market Analytics by OPIS (Michael.Samueli@chemicalmarketanalytics.com)