European Solar Prices Hold Firm Amid Uncertain Market

European photovoltaic (PV) module prices remain broadly stable in early April, but underlying conditions point to growing tension between policy-driven cost increases and subdued demand. While headline pricing suggests balance, transaction activity and supplier behaviour indicate a more fragile equilibrium.

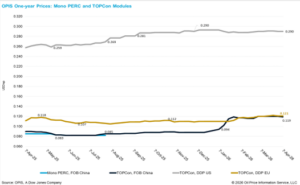

In Europe, Delivered Duty Paid (DDP) prices for imported TOPCon modules in the ≥600 wp segment are holding near €0.105/wp, with Tier-1 indications between €0.092/wp and €0.114/wp. Ex Works (EXW) prices for smaller ≤450 wp modules are assessed around €0.110/wp, with offers spanning €0.100/wp to €0.120/wp.

On the surface, price levels have shown limited movement in recent weeks. However, pricing has become increasingly negotiable, particularly for utility-scale projects, reflecting heightened competition amid weak demand.

Price Stability Masks Diverging Signals

The current environment reflects a disconnect between upstream cost movements and downstream pricing.

Across the supply chain, upstream inputs continue to weaken. Chinese polysilicon prices have fallen sharply, while wafer and cell prices remain under pressure due to high inventories and limited purchasing activity. In contrast, module prices in Europe have remained stable and, in some segments, increased since the start of the year. Rooftop modules have seen more pronounced gains, reflecting tighter availability.

Market sources attribute this divergence to policy and timing effects. The removal of China’s export tax rebate from April 1 has raised effective export costs, while front-loaded procurement in Q1 has reduced near-term buying interest. As a result, suppliers are balancing higher cost structures against weaker demand, limiting price adjustments.

Demand Remains Subdued

Despite supportive macro conditions, including elevated fossil fuel prices and continued policy backing, PV demand in Europe remains muted.

Residential and commercial buyers are adopting a cautious approach, delaying investment decisions amid economic uncertainty. Utility-scale demand remains fragile, with grid constraints, permitting delays and financing challenges slowing deployment.

At the same time, the residential segment shows relative resilience. Demand has normalised and is increasingly driven by self-consumption economics rather than subsidies, supporting pricing in smaller-format modules.

Policy, Procurement Reshape the Market

Recent policy developments are playing a central role in shaping pricing dynamics.

The removal of China’s export tax rebate has introduced a structural shift, raising the cost base for exporters. However, weak international demand is limiting pass-through, with some manufacturers absorbing part of the impact to remain competitive.

In parallel, European procurement is evolving. Greater emphasis on traceability, compliance and ESG standards is shifting purchasing decisions away from pure price considerations. This transition is adding complexity and contributing to a more segmented market structure.

Geopolitics Reinforce Solar’s Strategic Role in Europe

The ongoing tensions in the Middle East, and their impact on oil and gas markets, have renewed focus on energy security across the region. Rising fossil fuel costs have strengthened the relative competitiveness of solar, while policymakers increasingly frame renewable deployment as a means of reducing dependence on imported energy.

For developers and policymakers, the current environment underscores the importance of balancing short-term cost pressures with long-term strategic objectives. While freight logistics and input cost volatility may introduce near-term challenges, the broader direction remains firmly supportive of solar expansion.

Outlook: Stability with Downside Risk

The European solar market is increasingly shaped by overlapping forces. Policy changes and supply chain disruptions are adding to sellers’ cost structures, which may slow the rate of price decline.

Longer term, structural drivers remain intact, but the market is entering a more complex phase where pricing is influenced as much by policy and geopolitics as by supply and demand.

OPIS, a Dow Jones company, is a world-leading provider of news, data, analysis and consulting for the energy, chemical and environmental commodity markets. OPIS Global Solar Markets extends this expertise to the full solar value chain, delivering pricing aligned with the International Organization of Securities Commissions (IOSCO) from polysilicon and wafers to cells and finished modules, along with regional benchmarks for Asia, Europe and the U.S.

Subscribers receive a weekly PDF with price assessments, historical data and expert insight, plus breaking news on market-moving developments. The service also includes the Solar Policy Tracker, covering key regulatory shifts across the U.S., Europe and India — including India’s ALMM — with clear analysis of policy impact and industry reaction.