The Caribbean and South American Methanol Pivot: Balancing Traditional Supply with Green Ambition

The South American methanol market presents a striking paradox: the region is a global supply powerhouse yet is challenged by internal constraints and shifting policy.

South America represented over 7% of global supply in 2025. However, in terms of consumption it remains one of the world’s smaller regional markets, accounting for approximately 3% of total global demand last year, driven largely by Brazil’s large biodiesel sector.

The methanol supply landscape in the Caribbean and South America is highly concentrated. Trinidad is the largest exporter, and nearly all its output goes to West Europe (34%), mainland China (21%), the United States (16%), and Northeast Asia (14%). Similarly, Venezuela exports about 90% of its output to West Europe (33%), mainland China (20%), Brazil (21%) and the United States (12%). Meanwhile, Chile exports about 90% of its production, primarily to Brazil (71%) and mainland China (28%). This export reliance faces significant new barriers, as the 15% US tariff on Trinidad and Venezuela could force these two countries to redirect some of their exports away from the United States, further prioritizing European and Northeast Asian destinations that have a higher cost to serve. Argentina’s production is regionally focused, with the country exporting 40% of its output to other countries within the region, such as Brazil.

Despite this collective export strength, capacity stability is uneven. Trinidad saw a net capacity loss in 2024. Venezuela has seen no new capacity since 2010. Chile’s current capacity is lower than its historical peak after Methanex strategically moved two plants to the US where natural gas feedstock is cheaper and more abundant.

The structural supply challenge in the Caribbean and South America boils down to natural gas availability and supply reliability. Ultimately, this feedstock insecurity is the primary factor preventing the region from maximizing its methanol production and achieving consistent supply.

Argentina’s stagnant methanol capacity has seen no major development since 2002. The nation is poised for a major energy shift, however. Natural gas production is nearing record highs, largely driven by the Vaca Muerta shale formation, the world’s second-largest non-conventional gas resource. This growth is transforming Argentina into a potential future LNG exporter. Vast domestic natural gas supply could unlock new opportunities for methanol production, potentially reversing decades of stagnation.

Trinidadian methanol output remains severely constrained by persistent natural gas supply limitations, stemming from a 60% decline in production since 2010 due to the maturity of its existing fields. This limited resource is subject to intense competition, as local producers must allocate supply between National Gas Company (in charge of domestic sales and distribution of natural gas) and their own high-value LNG export operations, keeping the petrochemical sector vulnerable to ongoing curtailments. The LNG, ammonia and methanol industries compete for natural gas supply. The short-term outlook for Trinidad is defined by major investments aimed at boosting supply, with targeted start around 2027.

Venezuela holds massive natural gas reserves which, as stated by Ente Nacional del Gas Venezuela (ENAGS), total approximately 195 billion cubic feet, ranking it as the eighth largest holder globally and the largest in Latin America. But the country’s ability to utilize this resource is severely constrained. Although 81% of these reserves are associated gas (found alongside oil), production has plummeted 50% by 2021, according to the EIA, largely due to systemic issues like inadequate infrastructure, a lack of technical expertise, US economic sanctions, and limited foreign investment. Compounding these problems, the subsidized domestic natural gas prices limit investment interest, and the recent drop in crude oil output has inherently restricted gas production, thus crippling the country’s ability to utilize its vast reserves for revenue generation. Following the ousting of President Nicolás Maduro on 3 January 2026, Venezuelan methanol’s operations continued to operate normally. The significant rollback of US sanctions in early 2026 has allowed major energy companies to resume gas projects in Venezuela. However, despite this optimism, regional methanol production is expected to remain constrained by natural gas curtailments until Trinidad’s new volumes arrive in 2027.

Venezuela holds massive natural gas reserves which, as stated by Ente Nacional del Gas Venezuela (ENAGS), total approximately 195 billion cubic feet, ranking it as the eighth largest holder globally and the largest in Latin America. But the country’s ability to utilize this resource is severely constrained. Although 81% of these reserves are associated gas (found alongside oil), production has plummeted 50% by 2021, according to the EIA, largely due to systemic issues like inadequate infrastructure, a lack of technical expertise, US economic sanctions, and limited foreign investment. Compounding these problems, the subsidized domestic natural gas prices limit investment interest, and the recent drop in crude oil output has inherently restricted gas production, thus crippling the country’s ability to utilize its vast reserves for revenue generation. Following the ousting of President Nicolás Maduro on 3 January 2026, Venezuelan methanol’s operations continued to operate normally. The significant rollback of US sanctions in early 2026 has allowed major energy companies to resume gas projects in Venezuela. However, despite this optimism, regional methanol production is expected to remain constrained by natural gas curtailments until Trinidad’s new volumes arrive in 2027.

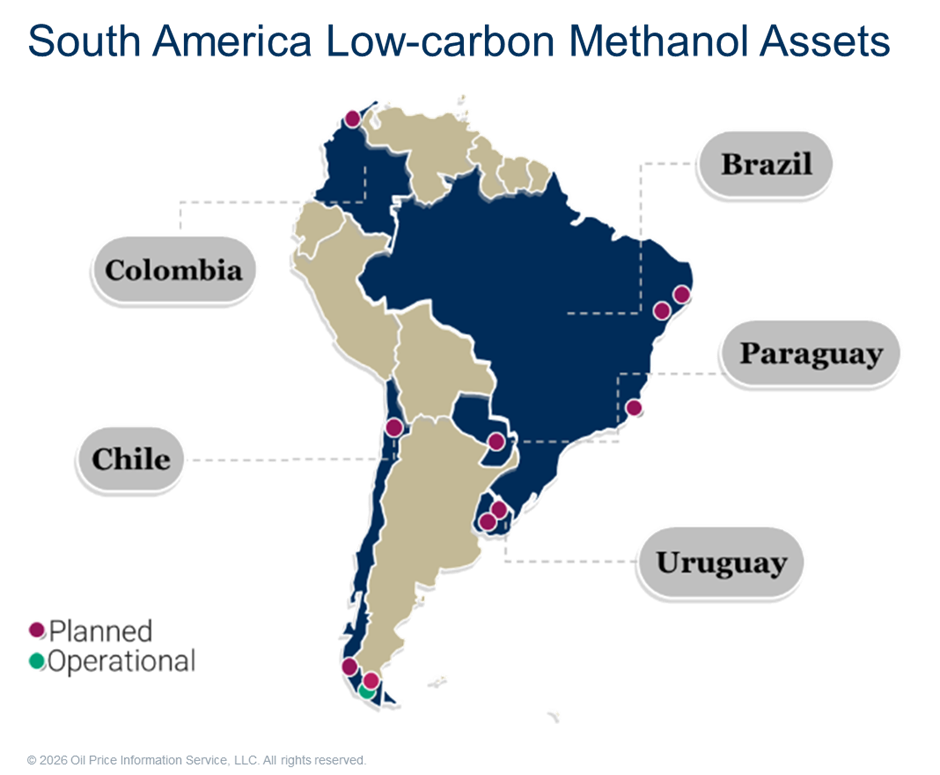

The future of South America’s supply could find some relief through its ability to transition to low-carbon methanol. Of the more than 40 low-carbon projects announced across the Americas, approximately ten are slated for South America, focused entirely on e-methanol (using renewable hydrogen and captured CO2). This is vital given the stagnation of conventional grey capacity. HIF Global, the only producer of low-carbon methanol in the region, running a facility in Chile, is providing the blueprint. HIF is planning further expansion into Uruguay, Brazil, and Chile. Other significant early-stage projects include GoVerde Energia’s planned methanol/ammonia hub in Brazil and Parafuel’s project in Paraguay. Success is not guaranteed, however; aside from HIF, none of these projects has reached a Final Investment Decision (FID), facing high barriers such as complex permitting and ensuring a stable, affordable supply of green hydrogen. The region’s ability to overcome these development hurdles will determine its success in the global decarbonization race.

The Middle East conflict is having a significant, though indirect, impact on South American methanol supply. While the overall region produces all the methanol needed to meet demand requirements, the global supply vacuum caused by tightness of supply in Europe and Asia is fundamentally altering trade flows and pricing in the Southern Hemisphere.

– Maia Dolan, Director, Methanol (maia.dolan@chemicalmarketanalytics.com)