2026 Preview: Asia’s LPG Market Braces for Oversupply as Demand Growth Stalls

Asia’s LPG market is set to face persistent oversupply in 2026, as fresh cargoes from key exporters enter the region against a backdrop of muted demand growth across major import markets. Prices are expected to remain under pressure, while key trade flows are likely to be reshaped.

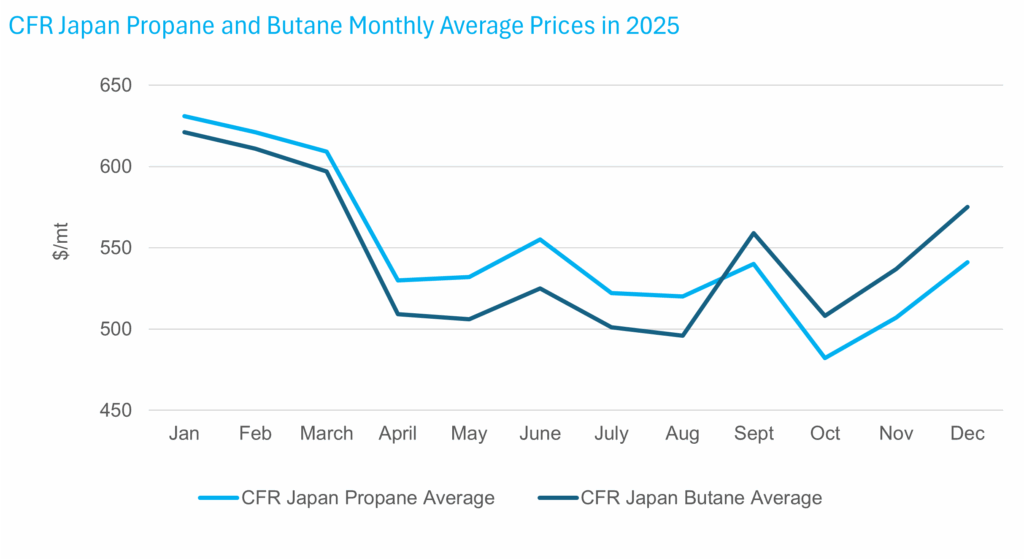

Price volatility in 2025

At the start of 2025, prices were above $600 per metric ton, supported by winter heating demand, but fell sharply in April after China imposed retaliatory tariffs on U.S. goods. CFR Japan propane and butane prices slid to averages of $530/mt and $509/mt, respectively, as concerns mounted over potential disruptions to U.S. LPG flows into China and a buildup of excess American cargoes in the region.

Prices weakened again in October, falling to their lowest levels of the year, after Saudi Aramco’s October contract prices came in below market expectations, triggering renewed bearish sentiment.

Oversupply amid rising export capacities

Oversupply concerns in 2026 are underpinned by rising LPG export capacities in the U.S. and the Middle East, two of Asia’s largest suppliers.

“Around 8 million mt to 10 million mt of additional U.S. LPG supply is expected to be directed toward Asia in 2026, equivalent to more than 170 additional cargoes,” an analyst said.

In the U.S., Enterprise Products Partners’ expansion of the Houston Ship Channel, adding 300,000 b/d of LPG export capacity, alongside Phase 2 of its Neches River Terminal development — allowing the facility to load up to 180,000 b/d of ethane and 360,000 b/d of propane — are scheduled to come online in 2026.

Middle Eastern supply is also set to rise. Aramco’s Jafurah gas field began initial production towards the end of 2025, with output expected to ramp up in the coming years, while QatarEnergy’s North Field expansion is slated for completion by mid-2026.

Muted Demand Across Key Asian Import Markets

Despite the increased supply, sources expect limited demand upside across Asia’s major LPG import markets. “There’s an anticipated supply glut in 2026, and this will put downward pressure on LPG prices,” a second analyst said.

China, Asia’s largest LPG importer, has been the key demand driver in recent years, fuelled by rapid expansions of its propane dehydrogenation sector. However, aggressive capacity additions have resulted in overcapacity, while downstream demand has softened.

China’s LPG imports totaled 30.05 million mt from January to October 2025, marginally higher than the 29.94 million mt recorded in the same period of 2024, according to customs data. Sources expect import growth to remain flat in 2026, with PDH demand having largely peaked.

“Only two new PDH units are scheduled to start up (in 2026) — Sinopec Zhenhai’s 600,000 mt/year plant and SP Chemicals’ 800,000 mt/year unit. This is lower than the five to six PDH start-ups seen (in China) in recent years,” a source said.

Japan and South Korea also saw slowing LPG demand in 2025. South Korea imported 8.53 million mt of LPG, down from 9.15 million mt a year earlier, while Japan’s imports edged down to 10.46 million mt from 10.48 million mt in 2024, Vortexa data shows.

Weak demand in both countries is expected to persist into 2026, largely due to ongoing consolidation in the petrochemical sector and reduced operating rates across plants.

South Korea has already embarked on a petrochemical overhaul, including the merger of crackers operated by Lotte Chemical Corp. and HD Hyundai Chemical Co. Further capacity rationalization is expected to curb demand for both LPG and naphtha feedstocks.

“Many South Korean crackers have already cut operating rates to around 70%–80% and could lower run rates further amid ongoing consolidation,” a Korean source said.

India is expected to be the only major import market in Asia with steady demand growth, driven primarily by the residential sector. National oil companies have already secured term deals to import a combined 2.2 million mt of U.S. LPG in 2026, which could help to absorb some of the additional supply.

Shift in Traditional Trade Flows

India’s push to diversify energy supply and increase purchases of U.S. LPG is expected to reshape traditional trade flows between key LPG exporters and Asian importers.

“Historically, China sourced LPG from the U.S. while India relied largely on the Middle East, but a switch could emerge in 2026 if India continues to increase U.S. intake,” a trader said. “Middle Eastern suppliers could lose Indian market share and redirect cargoes to China instead.”

A source from an Indian oil company has confirmed that discussions are underway for a second tender seeking U.S. LPG supply.

“All eyes are on India now,” said a second trader. “If the country takes in more U.S. volumes, Middle Eastern cargoes could be redistributed not just to China, but also to other Asian markets such as Japan and South Korea.”

–Reporting by Cheryl Lee, clee@opisnet.com; Editing by Mei-Hwen Wong, mwong@opisnet.com