Project REDD+ Struggles Amid Quality Push: Future of Voluntary Carbon Credits

Nearly two years after a major reckoning of forest conservation projects within the voluntary carbon market, REDD+ developers have managed to stay afloat. Some buyers are still retiring credits — but the market’s outlook remains uncertain.

“Voluntary is a dysfunctional market today. Very dysfunctional,”

-Pablo Fernandez, CEO of Ecosecurities

A Market in Search of Renewed Demand

REDD+ — short for Reducing Emissions from Deforestation and Forest Degradation — has faced a steep decline in demand. Prices plunged after widespread media and scientific criticism over inaccurate carbon accounting and poor engagement with local communities. While prices have begun to recover, they have yet to reach previous levels.

The OPIS REDD+ V21 credit average reached $14.25 per metric ton in 2023 before falling to $7.38 in April. By August, it climbed back to $9.71, settling at $8.99 per metric ton most recently.

According to Fernandez, prices between $5 and $10 per metric ton can’t cover the long-term costs of validation, verification, ratings, and other project incidentals.

Slow Progress on Quality and Methodologies

While prices are on an upward trajectory, work on quality initiatives has continued.

Verra is working to build out its consolidated REDD+ methodology, VM0048. Among other measures, the protocol calculates carbon reductions based on jurisdiction-wide deforestation, instead of comparing a project’s impact with a reference area chosen by its developer.

Verra is working to build out its consolidated REDD+ methodology, VM0048. Among other measures, the protocol calculates carbon reductions based on jurisdiction-wide deforestation, instead of comparing a project’s impact with a reference area chosen by its developer.

Progress, however, has been slow. As of June, only two maps — for the Brazilian states of Mato Grosso and Pará — were finalized, with six more available on a provisional basis. Verra did not respond to a request for comment regarding what maps had been finalized since.

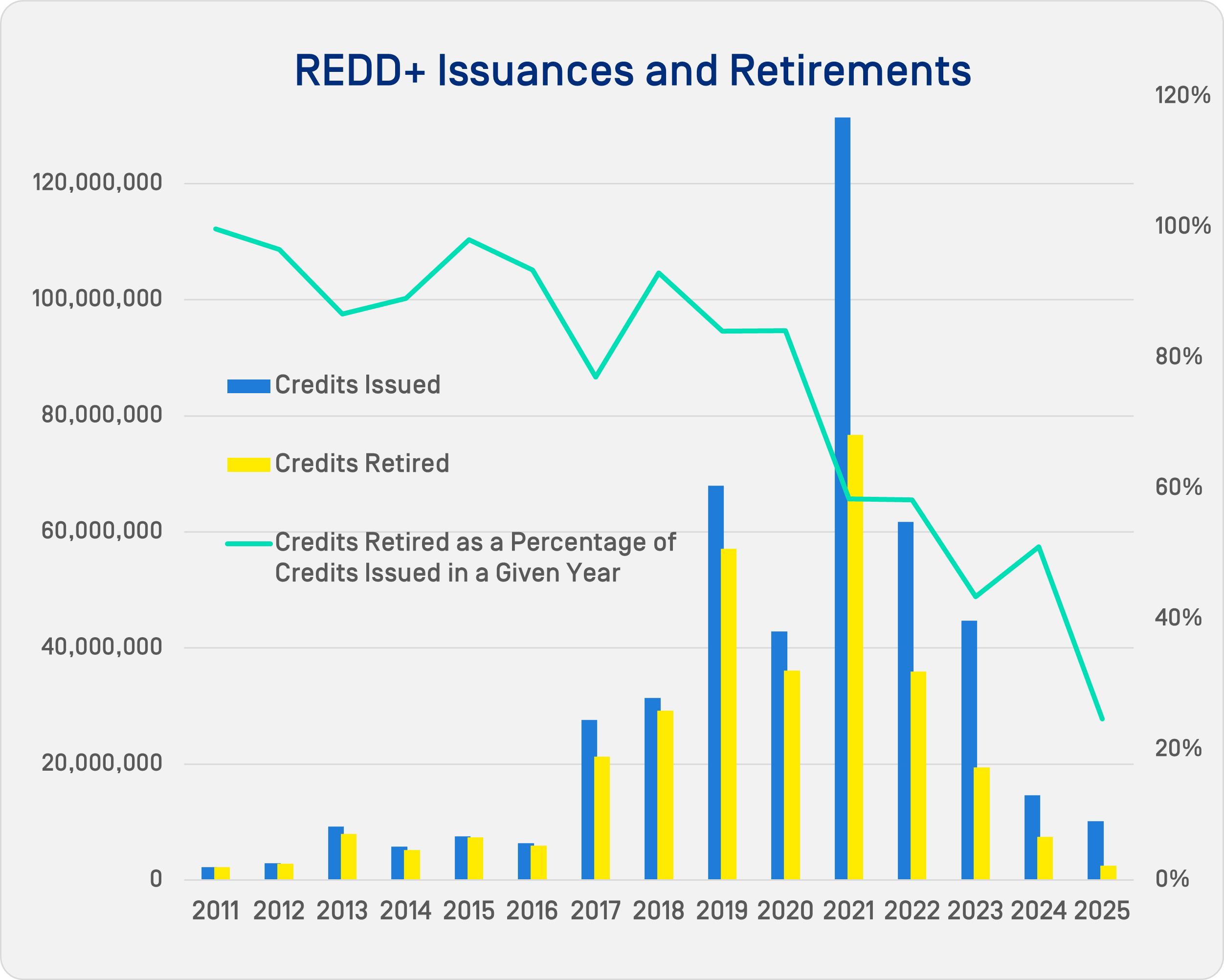

Meanwhile, the pace of REDD+ credit issuance has dropped dramatically. Volumes issued by Verra peaked at 131.4 million credits in 2021, falling to 61.7 million in 2022, 44.7 million in 2023, 14.6 million in 2024, and just 10.2 million so far in 2025.

Retirements have similarly declined — from 76.7 million in 2021 to 35.9 million in 2022, 19.4 million in 2023, 7.5 million in 2024 and just 2.5 million so far in 2025. Retirements have historically been highest at the end of the year and they will likely increase substantially by the end of December.

Meanwhile, Equitable Earth launched its new REDD+ methodology, M002, on Nov. 13. The protocol, along with Equitable Earth’s standard, seek to get around issues that have plagued the VCM in the past.

The registry does not charge a fee per credit issued, a mechanism that some believe has led to over-crediting in the past. It also conducts its own monitoring, reporting and verification, instead of leaving that task to project developers.

Equitable Earth also requires projects to promote biodiversity and publish transparent benefit sharing plans with local communities that support projects. The standard said projects protecting over 4 million hectares were moving toward certification.

For Some Projects, It’s Still Business as Usual

At Carbon Tanzania, co-founder Jo Anderson says long-term offtake agreements have helped protect the organization from REDD+ market volatility.

“We’re not market actors, we’re not financiers, we’re not bankers,” Anderson said. “We’re biologists, and the science tells us we have to protect forests, so we’re protecting forests.”

The company currently has three registered projects — two with Verra, one with Plan Vivo — and a fourth under development with Verra’s new methodology.

“There’s been a lot of noise around using nature in other ways to generate removals, which is the credit type now that is preferred by the market,” Anderson continued. “I don’t think much else has really changed in terms of what we do.

“In the meantime, we are looking carefully at how we can repurpose and readjust our sales strategy, but we’re not going to suddenly turn the organization inside out just to respond to a faddish market trend.”

Jurisdictional REDD+

While project-level REDD+ struggles, jurisdictional REDD+ (JREDD+) — which operates across entire states or countries — sits in an almost opposite position of project-based REDD+. A handful of governments have secured significant financial backing, with forward purchase agreements pricing credits between $5 and $15 per ton.

The LEAF Coalition, a JREDD+ buyers club, launched in 2021 with a $1 billion advanced market commitment. The group has continued to sign emissions reduction purchase agreements. LEAF’s four ERPAs — with Ecuador, the Brazilian state of Pará, Ghana, and Costa Rica — total nearly $300 million.

“The focus since then has been on signing more deals with more countries and bringing in more demand from the private sector,” said Philip Brady, EVP of Marketing and Communications at Emergent, which manages LEAF’s JREDD+ transactions.

The agreement with Para signed in September 2024 valued credits at $15/mt, while the Ecuador offtake was at $10/mt.

“There just haven’t been enough transactions to really form a view of where the market is going,” Brady said. “If you look at JREDD+ in general, the [World Bank’s Forest Carbon Partnership Facility] is $5 per ton. The Initial LEAF price was $10 a ton, priority $15 a ton. So, we’re seeing LEAF has helped increase prices. Individual prices with individual jurisdictions, we wouldn’t comment on that. It’s up to the seller and the buyer to set the price between them.”

Still, none of these countries have delivered credits yet.

“All of these countries are going through this process for the first time,” Brady explained. “It’s complex. It’s going to take time.”

The COP30 United Nations Climate Change Conference in Belém, Brazil also saw a series of announcements supporting the development of JREDD+. The Scaling JREDD+ Coalition, an effort by the World Bank and the Initiative for Sustainable Forest Landscapes, launched, while Brazil and numerous companies issued a joint declaration of support for “jurisdictional forest protection and high-integrity carbon markets,” according to the group’s Nov. 13 news release.

While JREDD+ has seen growing support, it remains a less-developed market than project REDD+.

Interplay Between JREDD+ and Compliance Markets

All LEAF agreements are tied to the Architecture for REDD+ Transactions (ART) registry. So far, only Guyana has issued credits through ART — and it has elected to target the market for Phase I of CORSIA, the UN’s carbon offset scheme for international aviation.

CORSIA’s first phase (2024–2026) could generate demand for up to 236 million credits, and Guyana’s 15.9 million credits is currently the only CORSIA-eligible supply. These credits have traded recently between $15.75 and $23.50 per ton, a premium over typical REDD+ prices.

But major shifts are expected before compliance comes due in Jan. 2028. Credits from Verra, Gold Standard, ACR, the Climate Action Reserve and the Global Carbon Council are all moving toward eligibility, and most airlines haven’t started retiring credits yet.

“Airlines don’t hedge fuel more than six months ahead,” Fernandez said. “Why would they hedge carbon three years ahead? They will almost all wait for 2027.”

Fernandez predicts that JREDD+ will increasingly serve compliance markets like CORSIA and Article 6, while project-level REDD+ remains in the voluntary space.

“Because you’re talking about compliance schemes, you end up having a premium. On the project side, they really require ratings nowadays. No rating, no interest.”

Will Demand Return to Project REDD+?

Mike Musgrave, CEO and co-founder of Newt Natural Capital, has helped advise many African REDD+ projects. But the company doesn’t have any REDD+ projects on contract currently.

“There’s a very low level of new REDD+ projects coming online because the financials just don’t make much sense,” he said.

According to Musgrave, REDD+ developers are facing “an ideological position around the monetization of nature which is fundamentally opposed to anything to do with monetizing carbon in a conservation type context.”

“If that’s the ideology, there’s nothing really the industry can do to fight back against that other than to cite the general failure of conservation to actually preserve any of these areas on a scale that is meaningful,” Musgrave said. “That ideological stance then gets applied to sometimes legitimate problems in a REDD+ project and leads some to conclude that the whole thing’s a waste of time. That it’s all one big scam and one big lie. Well, that’s quite an extreme position to take on any project, even the worst ones.”

Verra’s VM0048 methodology, with its jurisdiction-wide reference area, hopes to get around issues of over-crediting by taking a much more conservative approach to crediting. In some cases, that could reduce project issuances by as much as 70%, sources have told OPIS. Improved satellite and remote sensing tools are also making monitoring more precise. Still, total certainty is unrealistic.

Verra’s VM0048 methodology, with its jurisdiction-wide reference area, hopes to get around issues of over-crediting by taking a much more conservative approach to crediting. In some cases, that could reduce project issuances by as much as 70%, sources have told OPIS. Improved satellite and remote sensing tools are also making monitoring more precise. Still, total certainty is unrealistic.

“We’ll never reach a stage where we can LiDAR-scan every leaf and twig in real time,” Musgrave said. “We need to be doing this stuff now.”

In both Musgrave’s and Anderson’s views, uncertainty over outcomes is inherit in any REDD+ project.

“We can’t know what will happen in the future,” he said. “It will always be unknowable. In the end, it’s about reducing error — that’s what science is about.”

Some experts believe insurance mechanisms may help manage this uncertainty, though they can’t eliminate it.

“That’s the problem when I speak to the finance end,” Anderson said. “They find that uncomfortable.”