The Freight Squeeze: Why Record US LPG Exports Aren’t Telling the Whole Story

April 2026 was a month of contradictions for the U.S. LPG market. On paper, the opportunity was historic. The Mont Belvieu-CFR Japan arbitrage remained wide throughout the month, with the spread between U.S. and Asian propane staying well above pre-disruption levels.

However, the “screen arb” rarely tells the full story. While export volumes surged to new records, the cost of moving those barrels shifted from a routine expense to a dominant market force. By month-end, U.S. Gulf Coast (USGC) terminal fees had plummeted by roughly 70% from their early-April peak. When the arb says “go” but the netback says “wait,” the bottleneck is almost always in the water.

The Backdrop: A Gulf Sidelined

The Strait of Hormuz entered its ninth week of closure in April. The supply vacuum intensified as Saudi Aramco confirmed no May exports from its Juaymah NGL terminal, removing a critical piece of Middle East supply.

U.S. producers stepped into the breach. April exports out of the U.S. set a fresh record, eclipsing March’s highs. Enterprise’s Neches River terminal proved vital, ramping up flex-swing capacity to bridge the global demand gap. The supply was available; the challenge was the increasingly expensive logistics of moving it.

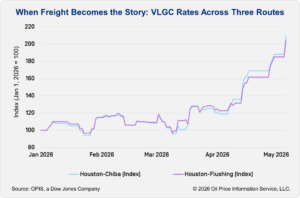

Freight: More Than Just a Route

Houston-Chiba VLGC freight surged approximately 55% month-over-month, reaching multi-year highs near $290/mt. This wasn’t an isolated spike.

Houston-Chiba VLGC freight surged approximately 55% month-over-month, reaching multi-year highs near $290/mt. This wasn’t an isolated spike.

- Houston-Flushing: Up ~48%

- Middle East-Japan: Up ~54%

The spike in the Middle East-Japan rate—despite the absence of Persian Gulf supply—is telling. It suggests the inflation isn’t just about U.S. export “pull.” Instead, we are seeing a global fleet tightness driven by structural shifts: fleet positioning, Cape of Good Hope rerouting, and a sudden scarcity of spot tonnage.

Panama or the Cape?

The Panama Canal has moved from a transit point to a strategic gamble. Auction fees hit record highs in April, with some slots reportedly fetching upwards of $4 million.

The market’s response is visible in the data. A growing share of U.S.-to-Asia cargoes are now bypassing the canal for the Cape of Good Hope. This adds roughly 14 days to a typical Ningbo-Houston voyage (from 30 to 44 days). Two extra weeks per voyage removes significant “effective” capacity from the global fleet, further thinning the spot market.

The Margin Squeeze at the Dock

The most immediate casualty of rising freight and canal costs has been the USGC export fee. Dropping 70% from early-April peaks, these fees have absorbed the pressure of the logistics premium.

For cargoes to keep moving at record volumes, the value chain had to give somewhere. In April, the dock took the hit. Shipping costs—whether paid via Panama auctions or absorbed as bunker fuel and time on the Cape route—now command the lion’s share of the arbitrage value.

Outlook: The Logistics Premium May Outlast the Disruption

The consensus view is that these pressures will unwind once the Persian Gulf reopens. We view the recovery path as significantly more complex.

A “reopened” Strait is only the first step. Damage assessments and facility restarts at Juaymah will carry their own timelines. Furthermore, shipping patterns possess their own inertia; voyage commitments and fleet positioning don’t pivot on a single headline.

Early May data suggests the squeeze is intensifying. Houston-Chiba freight continues to climb while terminal fees compress further. For traders and infrastructure owners, the message is clear: the logistics premium is no longer a temporary spike—it is the new baseline for the foreseeable future.