Volatile Freight Rates Muddle Global Solar Prices

Solar module prices around the world have moved in lockstep with Chinese prices for much of the past decade, which is no surprise given China’s dominance in solar manufacturing. The country accounts for over 80% of the world’s solar supply chain and this excludes its direct investments in other countries, especially in Southeast Asia, another major solar exporter.

But this relationship between FOB China prices and delivered prices is fraying. Thanks to volatile freight rates and a widening webwork of trade barriers, prices of solar modules loading from China and those delivering in the U.S. have been diverging.

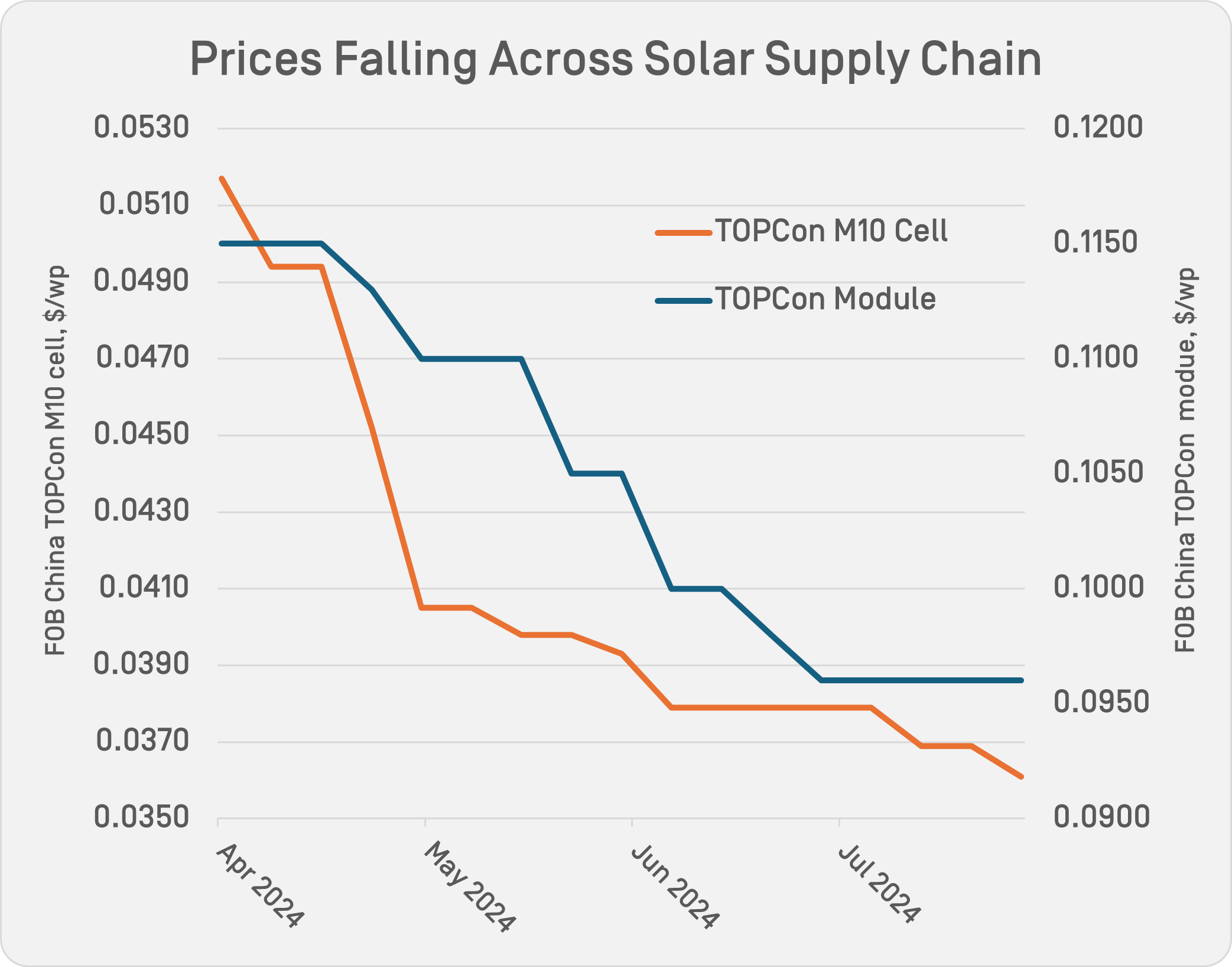

From April to July 2024, export prices of FOB China TOPCon M10 modules have fallen by 17% to $0.096 per watt peak (wp), the result of a Chinese solar industry struggling to arrest a downward spiral of growing overcapacity and ruinous price cuts.

From April to July 2024, export prices of FOB China TOPCon M10 modules have fallen by 17% to $0.096 per watt peak (wp), the result of a Chinese solar industry struggling to arrest a downward spiral of growing overcapacity and ruinous price cuts.

Over the same three-month period, however, prices of DPP US TOPCon modules have risen by 10% to $0.296/wp.

Freight volatility is a major factor behind the divergence. The Freightos Baltic Container Index (FBX), a weighted average of spot rates for 40-foot containers on 12 global trade lanes, has risen from around $1,330 per forty-foot equivalent unit (FEU) in February 2020 to over $11,000/FEU in September 2021, crashed back down to below $1,050/FEU in October 2023 before soaring back up to almost $5,200/FEU in July.

In the three years prior from 2017 to 2020, the FBX has stayed in a far narrower range of $1,040/FEU to $1,760/FEU.

Port congestions and geopolitical tensions that are rerouting shipping flows away from key shipping lanes help to explain this freight volatility. Such factors might seem transient, but as events of the past two years have shown, geopolitical flashpoints around the world can easily lead to shipping upheavals — possibly for extended periods.

The other factor behind the divergence between FOB China and delivered solar prices is the shift away from the free market ethos that has underpinned large swathes of global trade since the 1990s.

In place of unfettered free trade, countries are increasingly setting up barriers in the form of import quotas, tariffs and other exclusionary policies. China, with its dominance in solar and other manufacturing industries, has been a conspicuous casualty of this paradigm shift.

With terms like “onshoring” and “friend-shoring” now part of the global trade lexicon, such protectionism appears to be here to stay for now. The U.S., Europe and India, among others, have already promised billions of dollars in incentives and subsidies to build their own solar supply chains outside of China. Chinese manufacturers themselves are setting up factories in end-user markets, including in the U.S. and the Middle East.

All these developments call into question the relevance of FOB China prices as a universal, definitive reference for solar markets around the world.

Despite the growing protectionist shift, China’s massive production capacity continues to supply most solar markets in the world. It also remains streets ahead of any other country in terms of technological innovations and manufacturing capabilities.

But it is also true that freight volatility and trade barriers have decoupled FOB China prices from some of the key delivered markets in the west. Solar exporters have highlighted the difficulties of negotiating delivered prices for shipments delivering months ahead, especially when using FOB China prices as a reference that might not translate well into the eventual delivered price.

There is a precedent for such a price decoupling in the solar supply chain. China is by far the world’s largest producer of polysilicon, the main raw material for solar modules. But trade barriers in the west have resulted in a two-tiered market for Chinese and non-Chinese polysilicon.

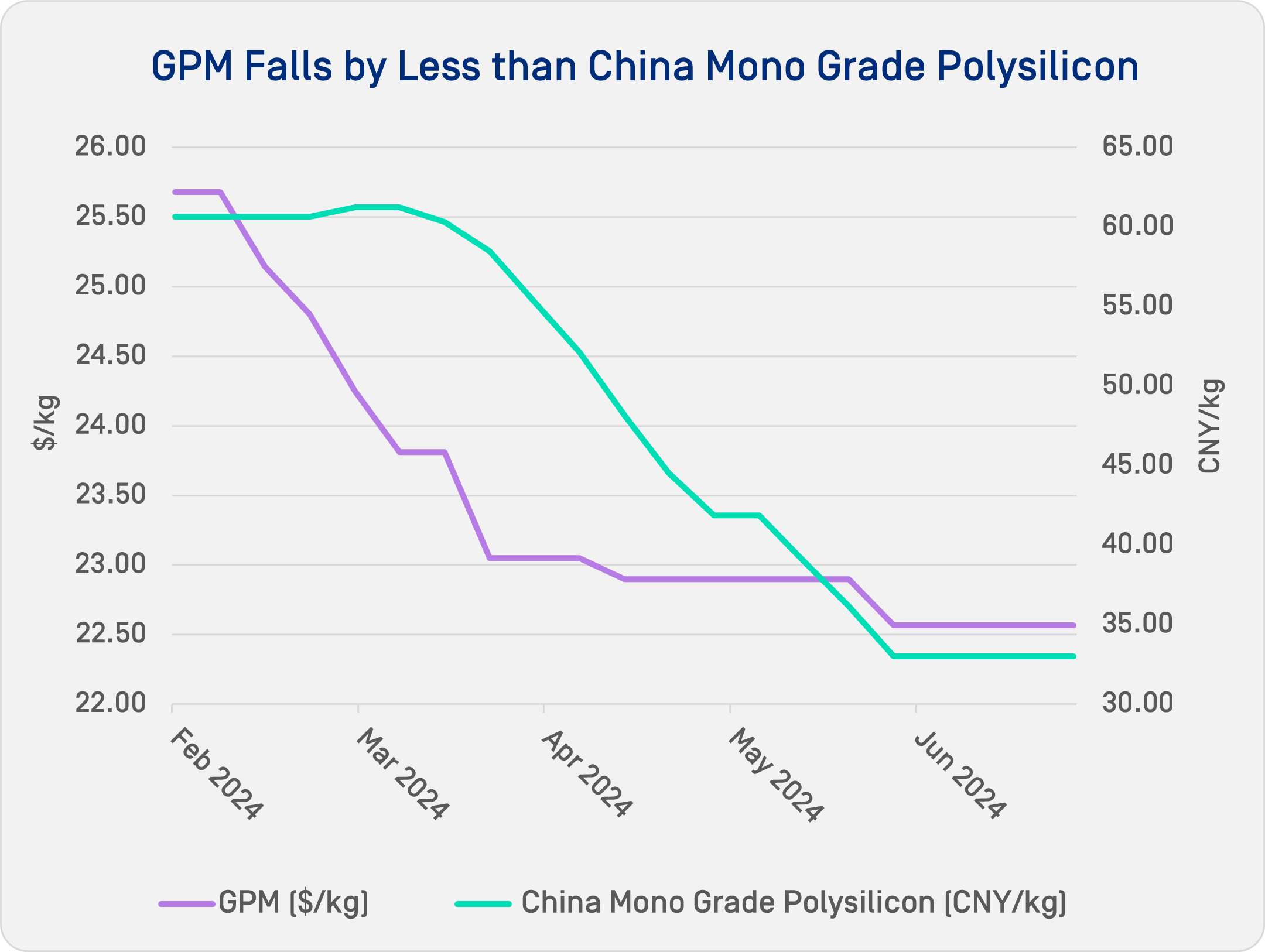

To address that pricing divergence, OPIS began to publish the Global Polysilicon Marker (GPM), a pioneering assessment in the industry to reflect the non-Chinese polysilicon market in 2022.

From January 2024 to Jul 2024, the GPM has fallen by around 14% while the domestic price of Chinese polysilicon has fallen by a far steeper 46%, reinforcing the fact that there is no single one-size-fits-all price assessment that can reflect all markets.

From January 2024 to Jul 2024, the GPM has fallen by around 14% while the domestic price of Chinese polysilicon has fallen by a far steeper 46%, reinforcing the fact that there is no single one-size-fits-all price assessment that can reflect all markets.

The divergence in module prices among regions should similarly be addressed by separate price assessments for the FOB China market and for the delivered markets in the U.S. and Europe.

And likewise, OPIS Global Solar Markets officially started spot assessments of TOPCon modules on a DDP Europe and DDP US basis, as well as a 12-month forward curve for DDP US TOPCon modules, from August 6.

The current trade and political climate suggests that the divarication in global module markets has yet to be fully played out. If policies to realize domestic solar manufacturing in major markets such as the U.S., Europe and India are successful, the links between FOB China and delivered module prices could only become more tenuous.