Assessing the Fallout of Middle East Conflict in the Nylon Markets

The 2026 Middle East conflict and the blockade of the Strait of Hormuz have catalyzed a systemic shock across the global petrochemical landscape. Although nylon manufacturing is largely insulated from the immediate conflict zone, the industry has still faced acute indirect pressure from elevated feedstock costs and raw material supply constraints, temporarily restructuring global trade flows for nylon intermediates and polymers.

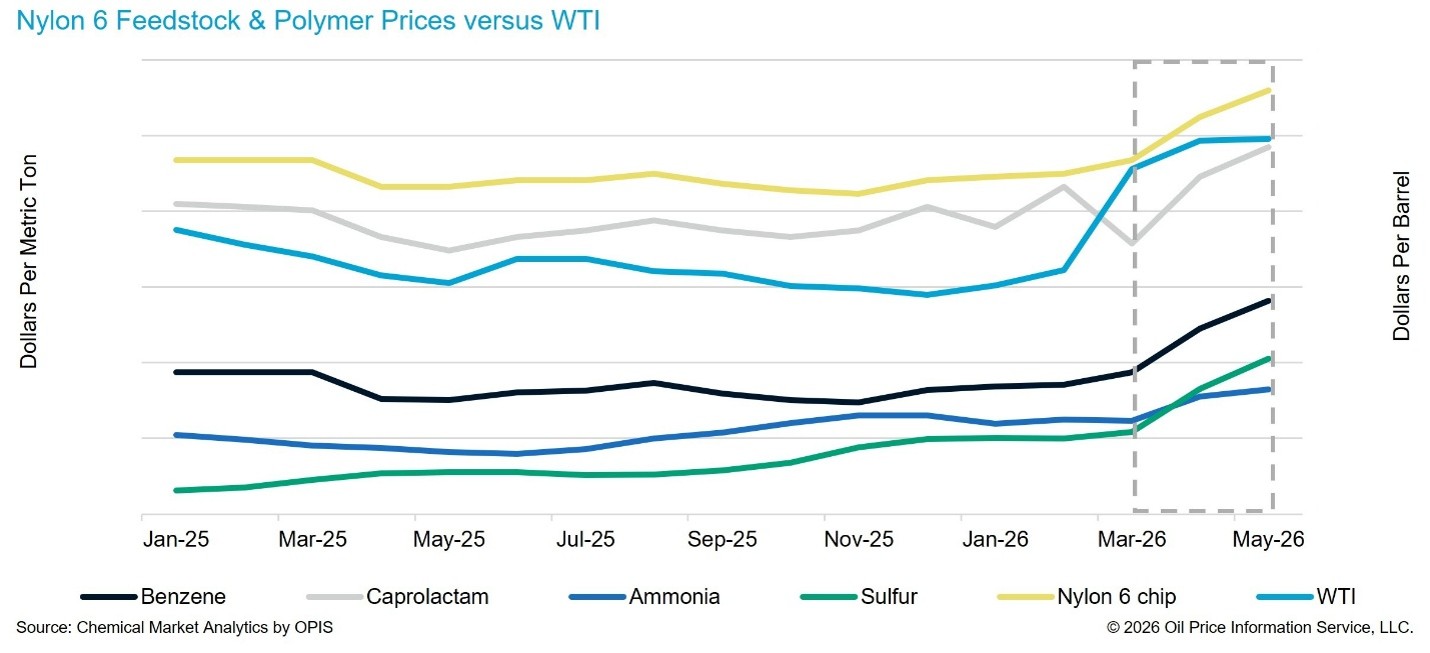

Supply disruptions have structurally elevated the global cost floor. In the nylon 6 market, feedstock benzene prices surged in direct response to spiking crude oil, alongside price climbs for key raw materials like sulfur and ammonia. These factors have contributed to a significant cost push for nylon 6 intermediates and polymers. Similarly, in the nylon 6,6 market, the cost of feedstocks like adipic acid and hexamethylenediamine (HMDA) has also been driven higher by rising benzene and ammonia prices and butadiene and propylene costs, respectively.

Amid escalating geopolitical friction and maritime logistics bottlenecks, the global nylon 6 industry has witnessed a temporary contraction in international trade flows. Because Western Europe is the primary exporter of nylon 6 chip to the Americas, this supply contraction—coupled with strong pre-buying activity driven by anticipated price hikes—has temporarily tightened availability in the American market, particularly for high-viscosity chip. However, the nylon 6 supply chain has not experienced the physical material shortages initially anticipated in West Europe due to flexible domestic sourcing. Meanwhile, caprolactam (CPL) supply in mainland China has faced constraints due to Middle Eastern material losses, specifically a severe sulfur shortage. However, supply remains more than adequate to fulfill offtakes, as downstream polymer producers have reduced operating rates in response to languishing demand.

Conversely, the nylon 6,6 industry experienced asymmetrical impacts. Asian cracker operating rates fell sharply due to a heavy reliance on Middle Eastern crude oil and naphtha imports, causing unplanned production cutbacks and reducing nylon 6,6 chip exports from mainland China. This has tightened availability and caused delivery delays in Western Europe. Meanwhile, the US nylon 6,6 supply chain has seen minimal impact from the conflict, allowing domestic suppliers to capture strong orders in export markets, though nylon 6,6 production has been constrained by economic pressures surrounding propylene and ongoing capacity restructuring.

Heightened uncertainty persists amid unfolding ceasefire negotiations, and the global energy landscape will need extended time to return to a pre-conflict state. CPL and nylon 6 chip are expected to remain well-supplied in Western Europe and Asia. The primary concern for the nylon 6 industry is that a persistent sulfur shortage will constrain CPL production, and high sulfur prices will continue to squeeze the industry’s margins. In the nylon 6,6 industry, while supply in Asia has gradually improved, overall, nylon 6,6 production in Asia is expected to remain under sustained pressure.

Based on current feedstock costs and supply-demand projections, prices for nylon intermediates and polymers appear to have reached their near-term peak and are expected to face downward pressure. Moving forward, the industry will grapple with compressed margins, eventually reaching a delicate balance as sustained high prices continue to erode downstream demand.

-Meiko Woo, Executive Director, Aromatics & Fibers (Meiko.Woo@chemicalmarketanalytics.com)