Green Steel: Separating Promise from Probability

The latest edition of McCloskey’s Green Steel Profile (subscription required) covers over 200 projects focused on either establishing new green iron and steel production with low embedded greenhouse emissions, or on modernising existing facilities.

The data highlights distinct regional trends, including:

- The shift from BF-BOF to DRI/scrap-EAF technology in the EU,

- MENA’s focus on green DRI production,

- China’s emphasis on optimizing BF-BOF operations alongside launching new EAF installations, and

- Australia’s potential emergence as a DRI hub for Asian markets.

In this edition, we also sought to ascertain the degree of likelihood in the project pipeline (subscription required) list. We assessed each project and its implementation likelihood, assigning one of four probability scores to each project’s expected steel production. The four likelihoods we used were:

- Certain: Projects currently in the construction phase. This category also includes projects in the final preparation stage that are led by companies with a proven track record of timely delivery and have secured all necessary financing and permits.

- Likely: Projects formally confirmed by companies with regular progress updates. These projects are undergoing construction preparation (such as equipment procurement) and have clear timelines toward a launch date.

- Possible: Officially announced projects that have some sort of risk associated with them being finalised, due to either market shifts or to potential changes in timing, scale, or technology.

- Unlikely: Projects that are stalled. This category also includes dormant projects that have seen no public updates or investment activity for an extended period.

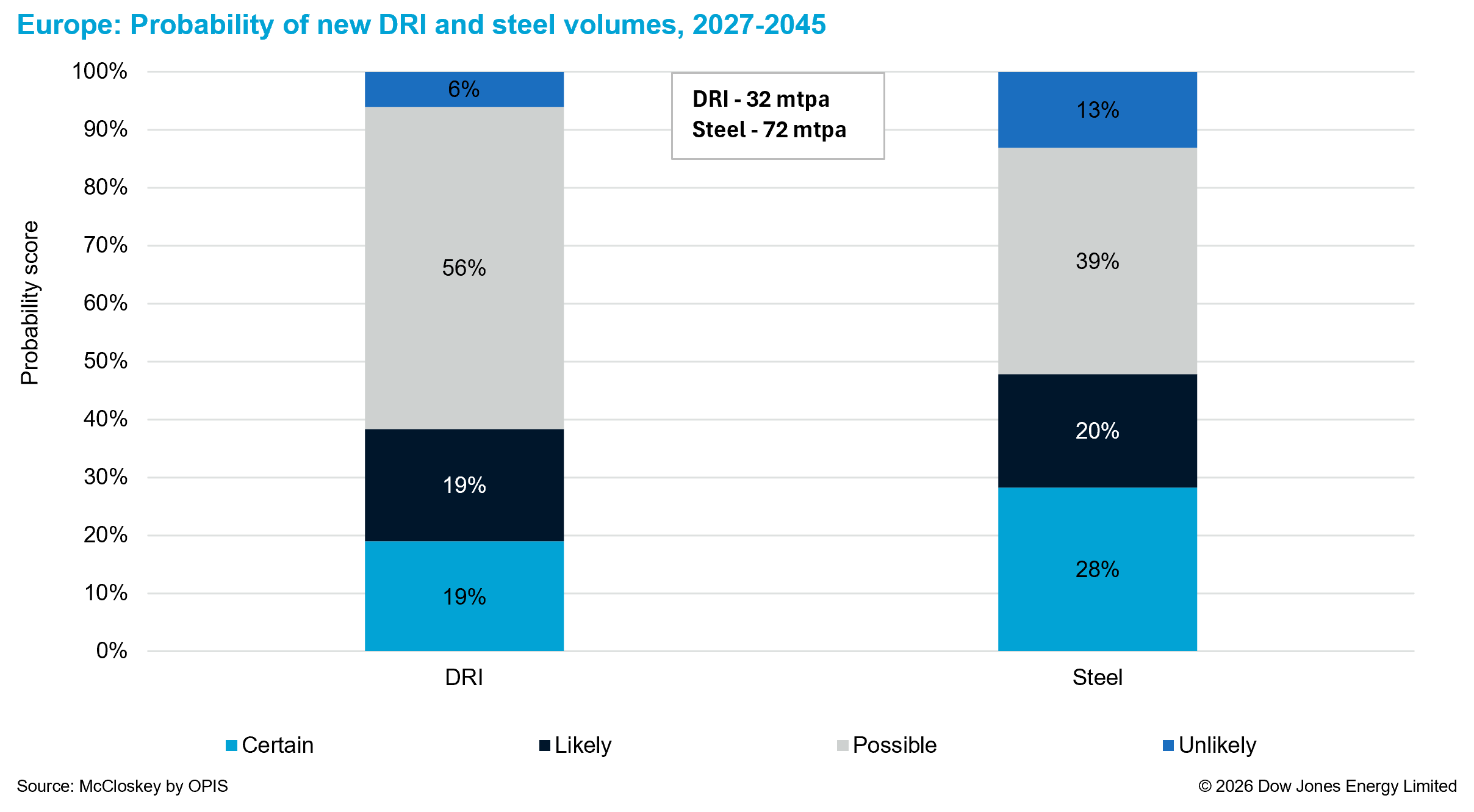

Europe

According to our estimates, European companies could add over 32 mtpa of DRI and more than 72 mtpa of green steel by 2045, with the majority of these volumes planned for the next five years.

The probability of realisation is higher for steel than for DRI projects. Several European steelmakers, such as ArcelorMittal, initially announced plans to produce DRI using natural gas or hydrogen but have since shelved these initiatives due to market conditions, opting instead for a partial transformation of the production chain: installing new EAFs to replace the BF-BOF route. This shift casts a shadow over other DRI projects in the region, reflecting broader investment trends as well as the high cost of natural gas, which is considered a transitional reducing agent for DRI production.

Figure 1

This explains why only around 38% of new DRI volumes in Europe are currently categorised as “Certain” and “Likely,” with these projects concentrated in the 2027–2029 window, while less likely volumes are scheduled for 2030 or later, reflecting later phases of decarbonisation projects that have not yet been finalised or fully configured.

For steel, “Certain” and “Likely” projects combined account for 48% of all new capacity, with the majority expected to reach the market within the next five years. Major EU steelmakers, such as ArcelorMittal, Salzgitter, Stahl-Holding-Saar, and Voestalpine, are moving forward with their previously announced transition from the BF-BOF to the EAF route, with the first phase largely slated for the end of the decade.

This move is driven by EU environmental regulations – specifically the ongoing phase-out of free emission allowances – and incentivised by new trade protection measures and the Carbon Border Adjustment Mechanism (CBAM).

Nonetheless, the “Possible” category continues to dominate the steel outlook for Europe, driven by massive volumes scheduled for beyond 2030, which remain highly tentative as many companies have yet to make final investment decisions on the configuration of the later stages of their net-zero transformation.

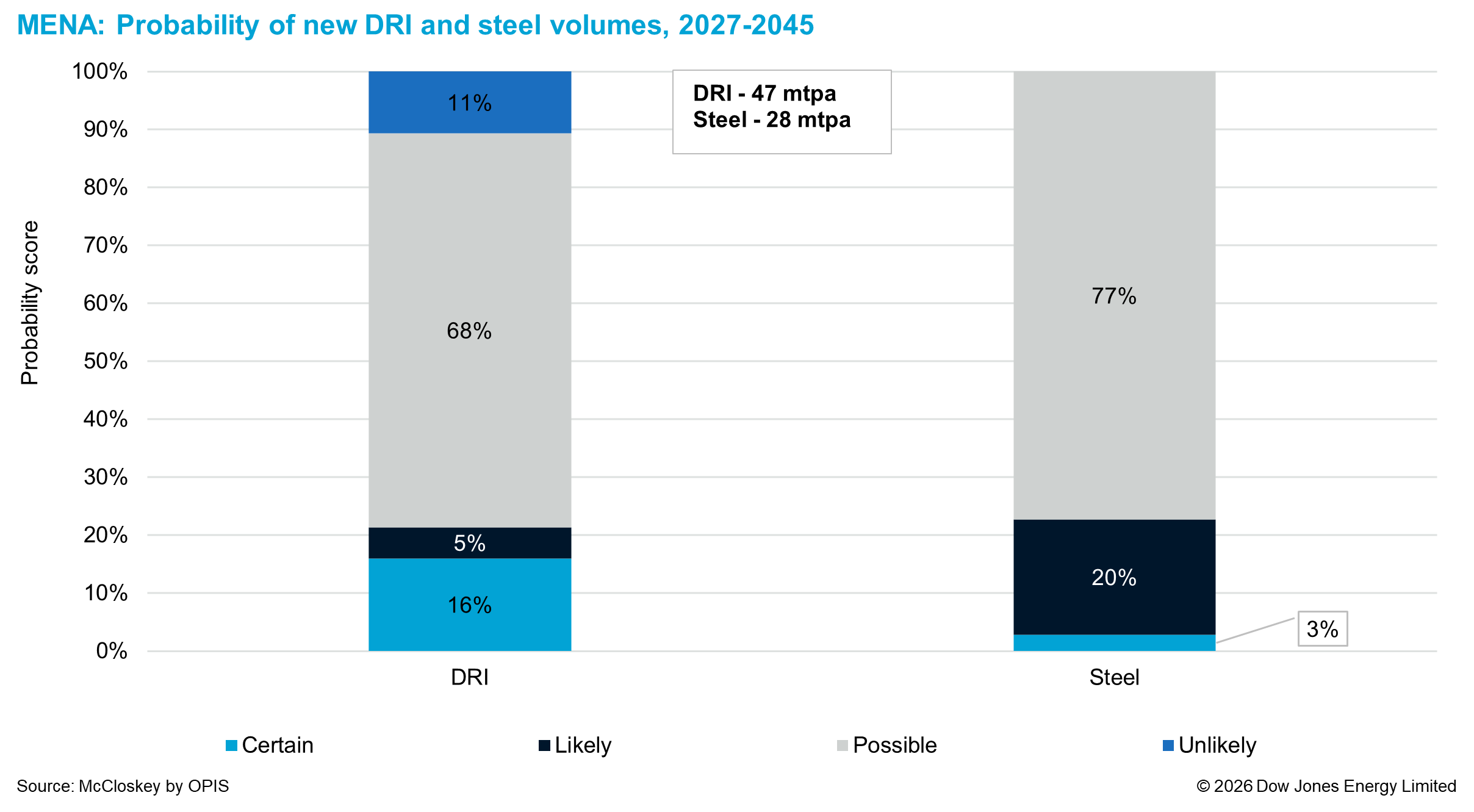

Middle East and North Africa

The MENA region is projected to generate significantly more green DRI than steel by 2040 – approximately 47 mtpa of sponge iron compared to 28 mtpa of steel, in the best-case scenario. This disparity is driven by the export-oriented nature of regional projects aiming to supply the global market with low-carbon metallics.

While MENA has long been a DRI powerhouse, fuelled by cheap natural gas, its output was historically reserved for local EAFs. Today, the region is pivoting toward becoming a strategic DRI exporter for European and Asian steelmakers. This transition involves scaling up existing sites and launching greenfield projects capable of switching from natural gas to hydrogen when it becomes available and cost competitive.

A prime example is Oman, where new production hubs in Sohar and Duqm aim to deliver 1 million tonnes of green hydrogen annually by 2030, accompanied by the greenfield DRI projects.

Figure 2

However, in contrast to Europe, the majority of volumes seem to carry question marks, and the “Possible” category dominates for DRI and steel volumes in the Middle East. This projection results from the high proportion of greenfield projects largely slated for 2030 and beyond, requiring massive capital investment and state support, with many projects still in the early stages of feasibility studies.

Furthermore, current geopolitical volatility in the Middle East weighs on expectations and is likely to expand the “zone of uncertainty” for investors, especially in countries dependent on supplies through the Strait of Hormuz, such as Saudi Arabia and the UAE. Recent Iranian strikes on two aluminium producers based in Bahrain and the UAE, and a retaliatory target list of six steel mills located on the Gulf Cooperation Council countries, highlights the risks for the local industry if the conflict reignites.

The region remains dependent on imports of iron ore and high-grade pellets, including those from LKAB, the EU’s largest iron ore producer. In March, the Swedish miner warned that it was suspending operations at one of its pelletizing plants at the Kiruna mine until November, citing delivery disruptions to Middle Eastern customers as a direct consequence of ongoing regional instability.

The Suez Canal has similarly acted as a supply chokepoint for European importers several times in recent years. The latest disruption resulting from the Iran war, which forced ships to reroute around the Cape of Good Hope, demonstrate that outsourcing supply chains—especially for a critical element like ironmaking—to volatile regions carries growing risk, and might force European steelmakers to review their long-term raw material sourcing plans.

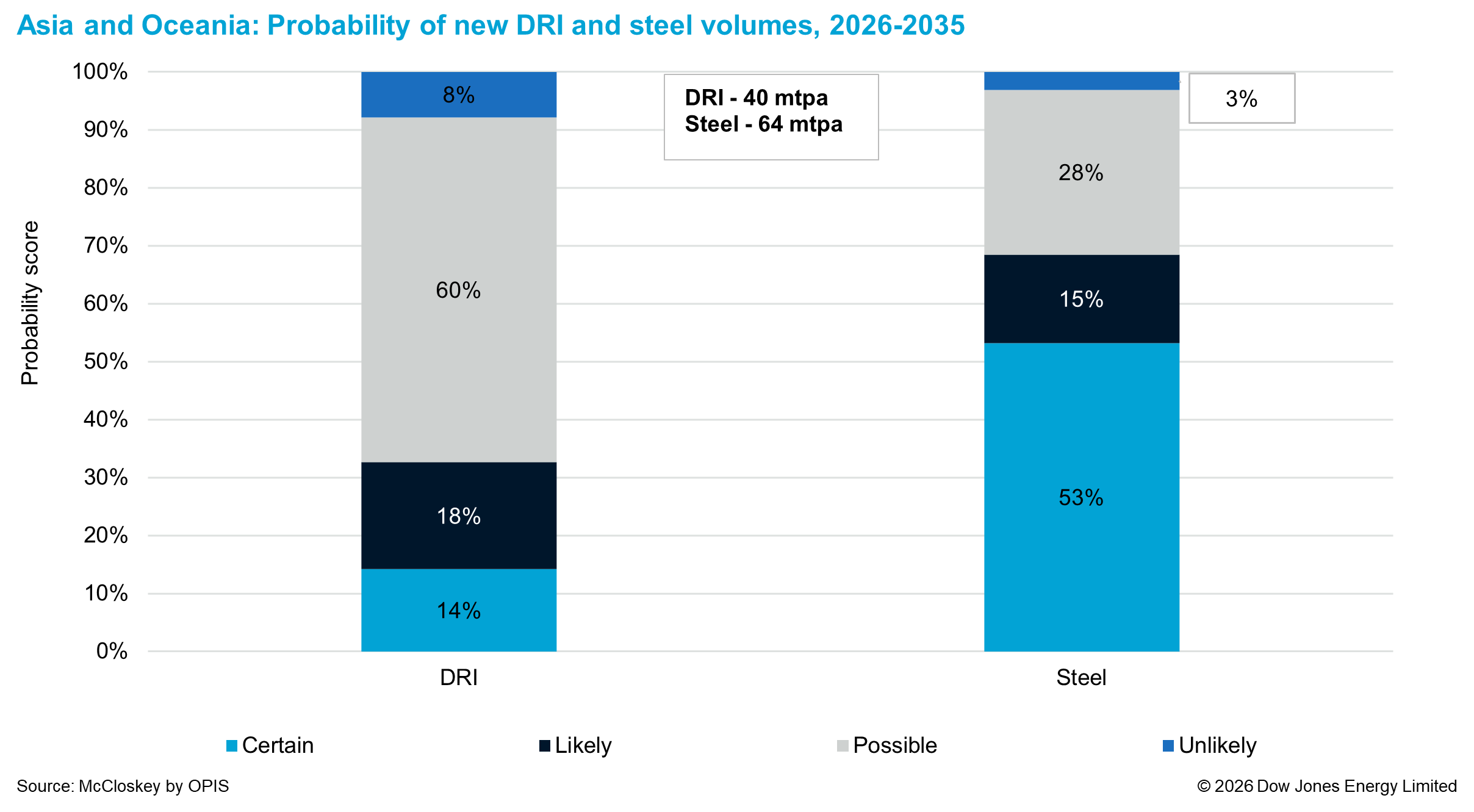

Asia and Oceania

Miners and steelmakers in Asia and Oceania are projected to deliver over 40 mtpa of DRI and more than 64 mtpa of green steel by 2035. The probability profiles for these two commodities diverge significantly: approximately 60% of DRI volumes fall into the “Possible” category, whereas steel projects appear to be more advanced, with around 68% rated as “Certain” or “Likely.” These figures are heavily influenced by specific national trends.

Figure 3

Nearly half of the projected DRI is expected to originate from iron-ore-rich Australia. With few exceptions, we categorise these volumes primarily as “Possible.” This reflects their greenfield nature, early development stages, and reliance on state support. A critical variable will be the advancement of technologies that enable the use of lower-grade iron ore in green steel production. Should this technological trend, currently confined to pilot- and trial-level projects, gain momentum, both volumes and the likelihood of realisation are poised to increase substantially.

China’s pipeline of new EAFs – either recently commissioned or under construction – underpins the confidence in the region’s new steel capacity coming online. A similar trend is evident in Japan and South Korea, though on a smaller scale and with later commissioning dates.

This momentum is primarily driven by China’s “dual carbon” strategy, which aims for peak carbon emissions by 2030. To accelerate this transition, the Chinese government’s 2026 steel work plan includes specific funding and long-term bonds to subsidise the decommissioning of older blast furnaces.

In Japan, the government is using its Green Transformation (GX) initiative to allocate billions of yen in subsidies to major steelmakers, specifically for large-scale EAF conversions. This financial support coincides with the 2026 launch of Japan’s GX-ETS emissions trading system, which imposes new carbon taxes on heavy industrial emitters.

South Korea is moving in a similar direction with its roadmap to carbon neutrality by 2050, which incorporates responsible procurement policies and strict emissions reduction targets for the steel industry. In all three countries, these government roadmaps are being accelerated by the need to remain competitive in the face of international regulations like the EU’s CBAM.

In contrast, the steel industry in Southeast Asia remains primarily focused on rapidly expanding its capacity to support its accelerated industrialisation and infrastructure needs. Nevertheless, based on announced plans, the region is expected to contribute nearly a third of Asia and Oceania’s green steel. Most of these volumes carry lower certainty than projects in China or Japan, with the exception of Vietnam, where the Xuan Thien Group has already begun construction of its 9.5 mtpa green steel complex in the Nghia Hung district.

India presents a different story. It has set a legally backed deadline of 2070 to achieve net-zero emissions, a longer horizon than that of other major economies. Domestic mills emit on average 2.65 tonnes of CO2 per tonne of steel (roughly a third above the global average), though the government aims to lower this intensity to 2 tonnes by 2035. To formalise this transition, the Ministry of Steel established a Green Steel Taxonomy, which officially certifies steel as “green” if its footprint falls below 2.2 tonnes per tonne of finished steel.

Simultaneously, however, India plans to nearly double its total steel capacity to 400 mtpa by 2035 to fuel infrastructure growth, an expansion driven primarily by new BF-BOF installations. But low-carbon projects are emerging; a prime example is Tata Steel’s commissioning of a 0.75 mtpa scrap-heavy EAF mill in Ludhiana in March 2026. Ultimately, as the world’s largest DRI producer, India’s development of solar power and green hydrogen is successfully laying the foundation for the eventual net-zero production of sponge iron.

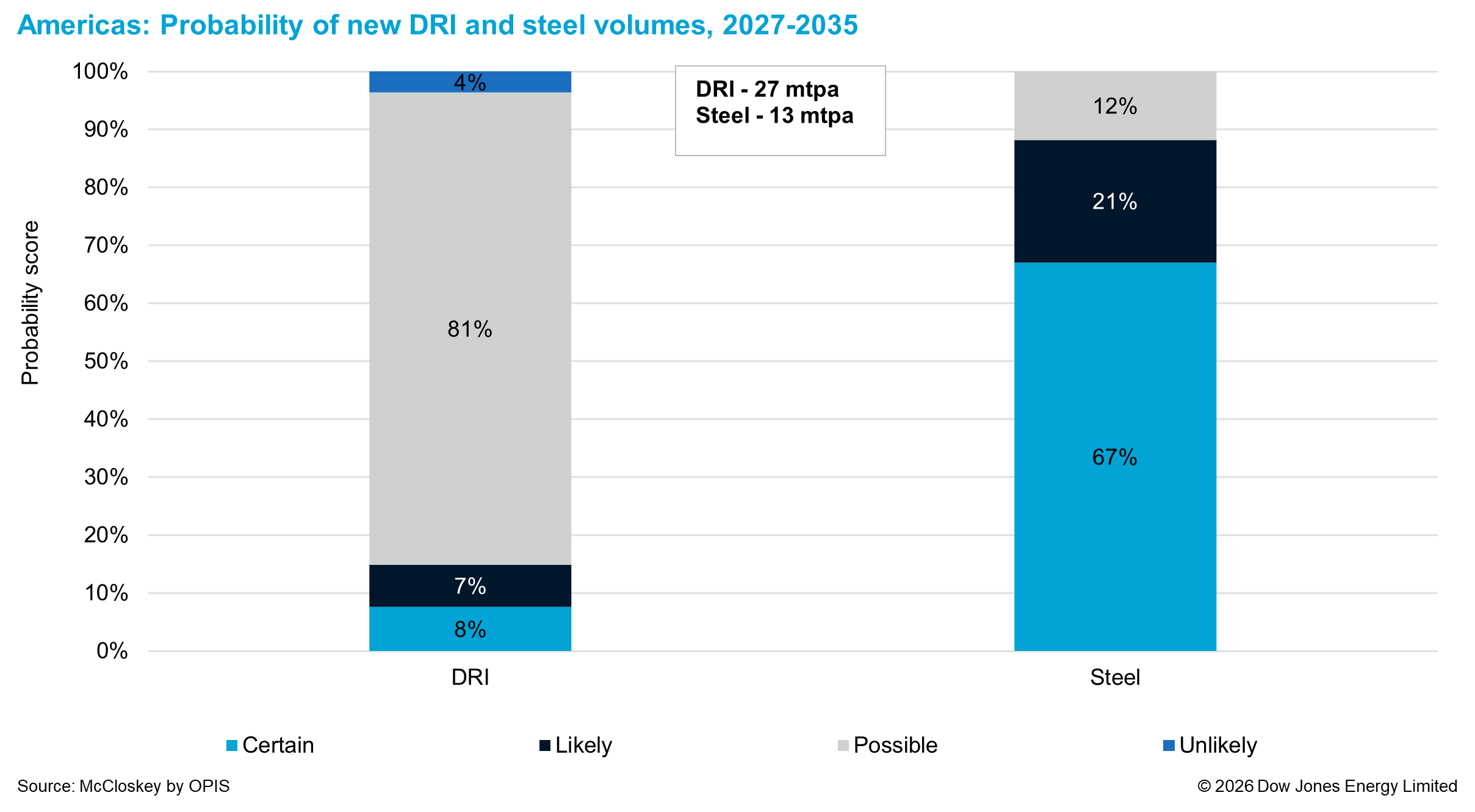

North and South America

In North America, most new steel and several DRI volumes carry high ratings: some are already commissioned and expected to reach full capacity by next year, while others are under construction. This is reflected in our assessment, which rates over 88% of new steel volumes as “Certain” or “Likely”.

However, the “Possible” category dominates the DRI outlook for the Americas at over 81%. This is partly due to an early development stage of the recently announced large-scale greenfield HBI project in Brazil.

The absolute figures for North and South America – 13 mtpa of new green steel and 27 mtpa of new DRI capacity – are lower than in other regions. This is primarily because the data is dominated by the US, the largest producer in the Americas, which already produces over 70% of its steel via the EAF route using a mix of scrap and metallics. Meanwhile, Brazil, the second-largest steelmaker on the continent, is utilising biochar and reforestation to offset carbon emissions.

Figure 4

As the emerging green iron and steel market continues to evolve, with new projects announced and existing initiatives adjusted, McCloskey will regularly review and update these probability assessments to reflect the latest market realities.

Further in-depth analysis of all publicly announced plans and ongoing projects can be found in the Global Green Steel Profile (subscription required) and in the latest update of the Green Steel Projects Database (subscription required) .

—Sergey Babichenko (sbabichenko@opisnet.com) & Marina Maliushkina (mmaliushkina@opisnet.com)