Middle East Conflict Winners and Losers: Polyolefins

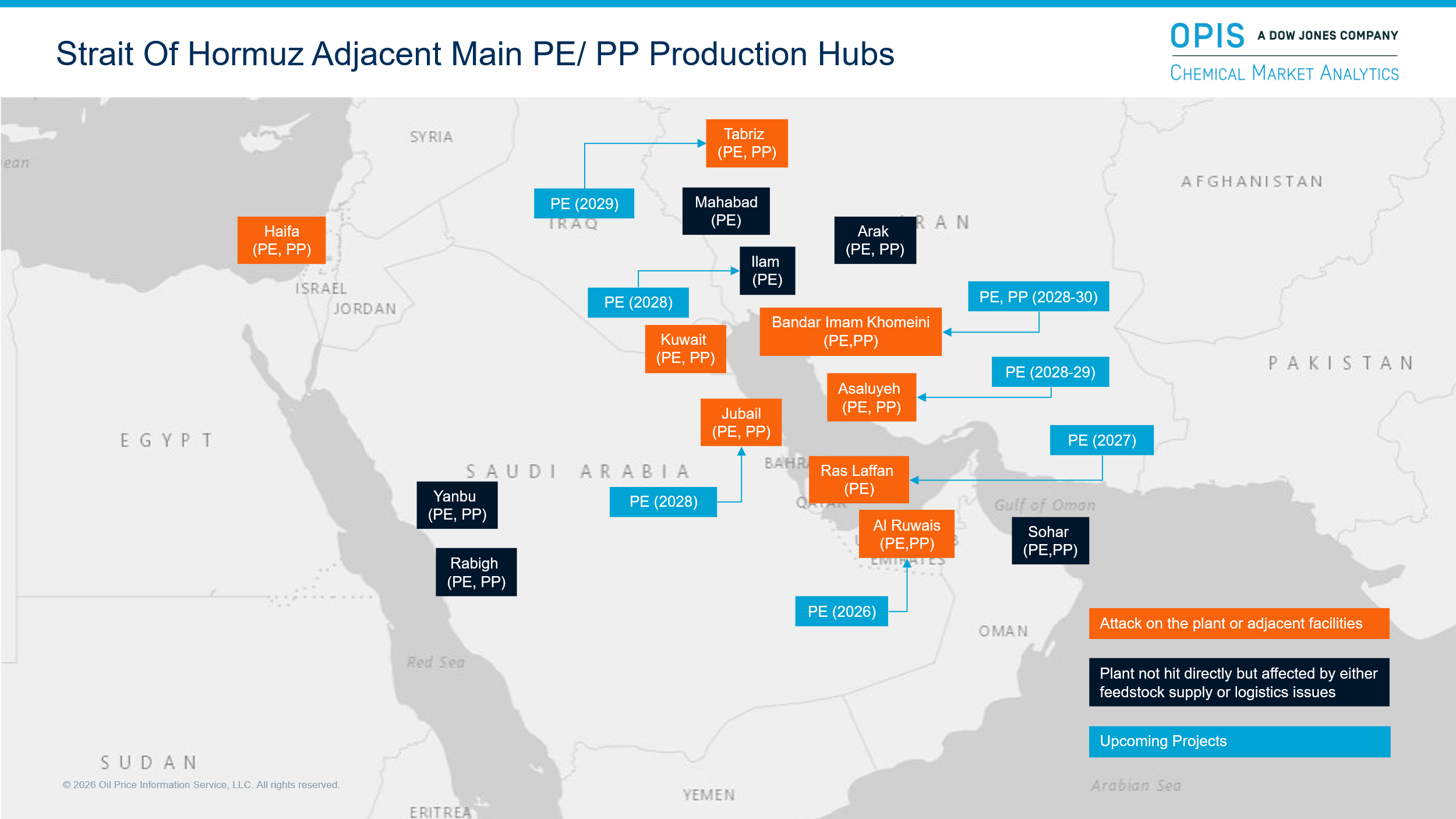

The Middle East region suffered significant physical damages that potentially include polyethylene (PE) and polypropylene (PP) plants and upstream facilities. Regional supply remains heavily curtailed due to feedstock shortages and inventory constraints, resulting in force majeure announcements and even forced some assets to shut down.

Elsewhere in the world, very limited spare capacity is available around the world to compensate for the loss of Middle East volumes in Europe. US volumes are yet to ramp-up and tight availability in Europe is already driving prices very high. In Europe, prices need to increase significantly to incentivize the spare capacity within the region to come on stream. At the time of writing European PE and PP operating rates are rising as the producers try to meet the surging demand, although the incremental volume may not be enough to offset the lost Middle East volume. Notably, this increase in domestic demand could be a major factor in rationalization decisions, some of which will likely be delayed in the current scenario.

In Mainland China, domestic production has been curtailed by feedstock disruptions. Lower resin imports further contributed to tight supply in the country, especially amid strong exports. Domestic spot prices rose sharply, but to a lesser extent than feedstock prices, pinching margins. Production may remain subdued due to feedstock constraints and government mandates prioritizing fuel output. There is also strong indication of likely demand destruction, especially in mainland China, India and the rest of Asia, driven by buyers’ resistance in accepting higher prices.

North America is the clear winner in the polyolefins market space. The regional producers, in particular US producers, are benefiting from skyrocketing export prices keeping pace with global markets. However, domestic downstream consumers are forced to keep pace with exports, and domestic prices are also on the rise. Seeing margin improvements, producers will likely ramp-up output to maximum limits, especially for PE. US PE operating rates were at 98% in March, according to the American Chemistry Council. Notably, this has not been the case in the last five years, so operational reliability could be an issue. For PP, propylene supply could become a limiting factor. Overall, North America has seen dramatically improved producer profitability compared to pre-conflict.

Even after return of peace, market will take time to normalize. Supply chain bottlenecks will take weeks if not months to reset even after the Strait of Hormuz opens.

Middle East production is also very unlikely to return to full capacity this year, as Engineering, Procurement & Construction (EPC) resources will be stretched. Similarly, projects under construction in the Middle East will face delays. Also of note, the geopolitical risk premium in the Middle East is expected to stay elevated, pushing up capital borrowing costs, which could hinder future investments.

– Joel Morales, Vice President, Plastics and Polymers Americas (Joel.MoralesJr@chemicalmarketanalytics.com); Kaushik Mitra, Executive Director, Polyolefins, EMEA (Kaushik.Mitra@chemicalmarketanalytics.com); Utpal Sheth, Vice President, Plastics Asia (Utpal.Sheth@chemicalmarketanalytics.com)