Shifts in the European Ethylene Market

A close look at the integration of the European ethylene market reveals the impact of recent plant closures, ownership changes, and capacity consolidation. In contrast to history, a growing number of the top producers in Europe are also buyers of ethylene. In fact, there are only a handful of companies considered to be substantial net sellers in Europe. For several smaller net sellers, the scale of their operations is far larger than their net position; variance in cracker and derivative utilization could easily shift these players from net sellers to buyers and vice versa.

Of greater impact on the market has been the underlying weakness in demand, which ensures a continued focus on rationalization within the industry. Recent steam cracker closures have pushed the region into a net short position. Consequently, structural imports are now necessary for derivative asset operations to be maintained.

Of greater impact on the market has been the underlying weakness in demand, which ensures a continued focus on rationalization within the industry. Recent steam cracker closures have pushed the region into a net short position. Consequently, structural imports are now necessary for derivative asset operations to be maintained.

When considering the dynamics of the integrated versus merchant market, the long-term preference for players to integrate between steam crackers and derivatives has ensured that most of the ethylene produced is consumed captively, both geographically and from a market perspective. However, from a market perspective and considering the influence on pricing dynamics, the net position is the most critical aspect, as it determines the role that players have in the market. Ongoing capacity closures and the idling of assets have affected the size of the merchant market over the past year, with more changes expected in the future.

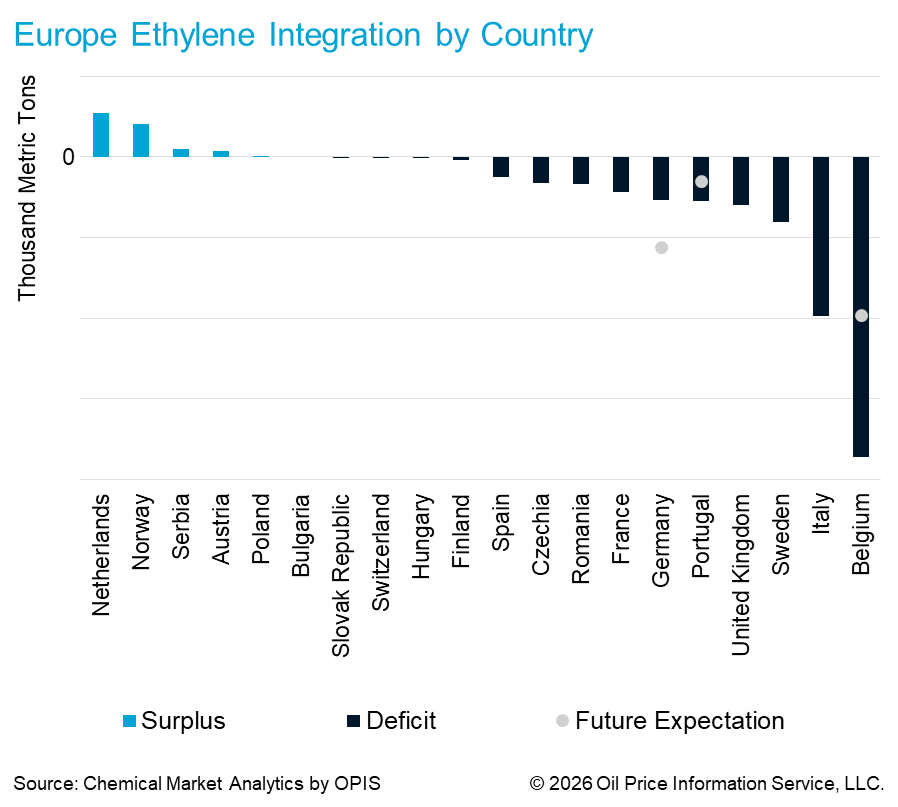

These shifts are also highly visible from a geographic perspective. Even though ethylene is a gas and difficult to transport, there is a large imbalance between different countries. Changes seen in company ownership have had no impact on country balances; it is only where expansions or closures occur that these balances shift. The ongoing reductions in supply capacity have pulled the entire European balance to a structurally very short position.

The European industry’s future is highly uncertain. A key catalyst for change will be upcoming steam cracker turnarounds, which for many may involve heavy investment in emission reduction as well as usual turnaround costs. This may tip the balance between the cost of staying in business and the cost of exit, in favour of shutdown. Furthermore, uncertainty around the European legislative environment and likely costs for continued carbon emissions make further closures highly probable.

However, the current crisis in the Middle East may give a lifeline to some European assets as legislators grow more concerned about the security of supply than has hitherto been the case. Some long-term benefits may be seen for the European ethylene industry should a sustained period of constraint be seen in Middle East exports.

–Matthew Thoelke, Vice President Olefins EMEA (Matthew.Thoelke@chemicalmarketanalytics.com)