Southeast Asia Olefins Market: Moving Away From the Middle East, Are There Alternatives?

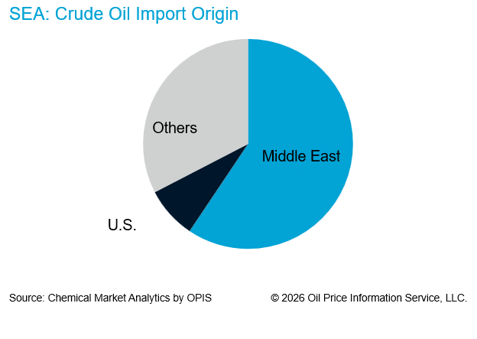

Following the escalation of military conflict between Iran and the United States/Israel in late February 2026, the sustained blockade of the Strait of Hormuz has emerged as the greatest threat to the Southeast Asian petrochemical market. The most direct impact is a severe reduction in cracker operating rates due to the cutoff of Middle Eastern crude and feedstock. Because refinery integration rates for regional crackers are relatively low, these facilities remain heavily dependent on naphtha imports from other regions to sustain their operations. Middle Eastern imports accounted for approximately 43% of the light naphtha sourced from outside the region as of 2025 and 59% of crude oil imports, making the continuity of these shipments a critical factor dictating regional operational status.

Undoubtedly, the escalating tensions have shifted the dynamics for Southeast Asian producers. Limited availability of raw materials has forced producers to curtail production rates and declare force majeure. In the last 12 months, operating rates have fallen from an average of 74% to currently hovering just above 50%. Meanwhile, monomer prices have risen rapidly to cover operating costs. However, producers are finding it difficult for production costs to catch up with feedstock costs, passing these costs on to the downstream to a sector already suffering with its own affordability constraints.

The 2026 crisis has accelerated the structural shift in how Southeast Asian crackers secure their feedstocks. The strategy is to move from a “lowest-cost sourcing” model to a “supply security and flexibility” framework. As Middle Eastern origin naphtha has tailed off, producers have looked elsewhere for steady and reliable sources of feedstocks to keep their assets running, driving an uptick in imports from alternative sources like the United States and Russia. Similarly, a shift is occurring in liquefied petroleum gas (LPG) supply. While LPG makes up a smaller fraction of the total cracker feedslate amongst SEA crackers, US LPG has steadily grown to become the largest import source, driven by US Gulf Coast export infrastructure.

As the Middle East conflict extends into its 15th week and begins to ease, some SEA producers are already diversifying feedstocks sources. Much of this diversification is for short covering near-term feedstocks. Producers are also evaluating permanent structural hedges against Middle Eastern supply volatility. Against this backdrop, the potential development of coal-to-chemicals and other domestically advantaged feedstock pathways is gaining renewed strategic attention as governments and producers seek to strengthen supply chain resilience and secure stable olefins and derivative supply during future disruptions. If energy security becomes a greater policy priority, SEA’s olefins market could experience structural shifts through increased refinery-petrochemical integration, alternative feedstock investments, and changing regional trade flows, while placing further pressure on higher-cost standalone naphtha crackers already challenged by global oversupply and weak margins.

As the Middle East conflict extends into its 15th week and begins to ease, some SEA producers are already diversifying feedstocks sources. Much of this diversification is for short covering near-term feedstocks. Producers are also evaluating permanent structural hedges against Middle Eastern supply volatility. Against this backdrop, the potential development of coal-to-chemicals and other domestically advantaged feedstock pathways is gaining renewed strategic attention as governments and producers seek to strengthen supply chain resilience and secure stable olefins and derivative supply during future disruptions. If energy security becomes a greater policy priority, SEA’s olefins market could experience structural shifts through increased refinery-petrochemical integration, alternative feedstock investments, and changing regional trade flows, while placing further pressure on higher-cost standalone naphtha crackers already challenged by global oversupply and weak margins.

The movement to reduce dependence on Middle Eastern feedstock is in its early stages, but the current crisis has made this strategic shift irreversible. Even if regional tensions eventually ease, baseline energy prices are expected to remain elevated due to extensive infrastructure damage, fundamentally altering regional processing economics. Over the longer term, energy security-driven investments, market consolidation, and greater feedstock flexibility will redefine regional trade flows and accelerate the transition toward supply chain resilience.

-William Chen, Executive Director, Asia Light Olefins (william.chen@chemicalmarketanalytics.com)