Tariff Talk: Who are Chinese Leaders Meeting With?

“Short memory, must have a short memory”

– Midnight Oil

Much of our focus in Tariff Talk since it was launched almost half a year ago has been the United States, and in particular the international trade actions of President Trump. And rightly so since those are creating much of the uncertainty in the global economy today. There is significant press coverage of deals being worked on and deals being done. However, the US is not the only nation that has been engaging in heavy meeting and negotiation schedules; most other countries have been too, primarily with the aim of mitigate exposures to the actions of the US administration.

China’s activities in particular have caught some media interest, with some focus in particularly on President Xi visiting and hosting leaders from Asia and Australia. And China has announced that Russia, Southeast Asia, and Central Asia are key diplomatic priorities. We wanted to explore these activities in a bit more detail, so in this edition of Tariff Talk we take a look at what China has been doing, which countries its two main leaders – President Xi Jinping and also Premier Li Qiang – have been meeting with, and how these have evolved since the election of Donald Trump to a second term. We look at what themes emerge and discuss what the implications may be for commodities and commodity trade.

First – some surprising things:

The Chinese leaders have not had more meetings than they did in 2024 before Trump was elected. In the first half of 2025 they had 68 meetings with heads of state, exactly equalling the 68 over the same period in 2024. And those 68 meetings in the first half of this year were well down on the 138 meetings in 2H 2024, though that number was highly inflated by President Xi having a tour of Africa in Q3 2024 when he had 44 meetings with African heads of state.

Also surprising – Xi and Li only had 19 meetings in Q1 – right after Trump was elected. Lunar New Year is in Q1 and played a part no doubt, but the two had 29 meetings in Q1 2024. One wonders if travel strategies were being refined as China scrambled in the wake of Trump’s election the onset of the US-China trade war, leading to a lull in Q1. Things certainly accelerated in Q2, with President Xi having his busiest quarter of heads of state meetings in two years (excluding Q3 when the Africa tour happened), with 37 meetings (a typical quarter has around 25-30).

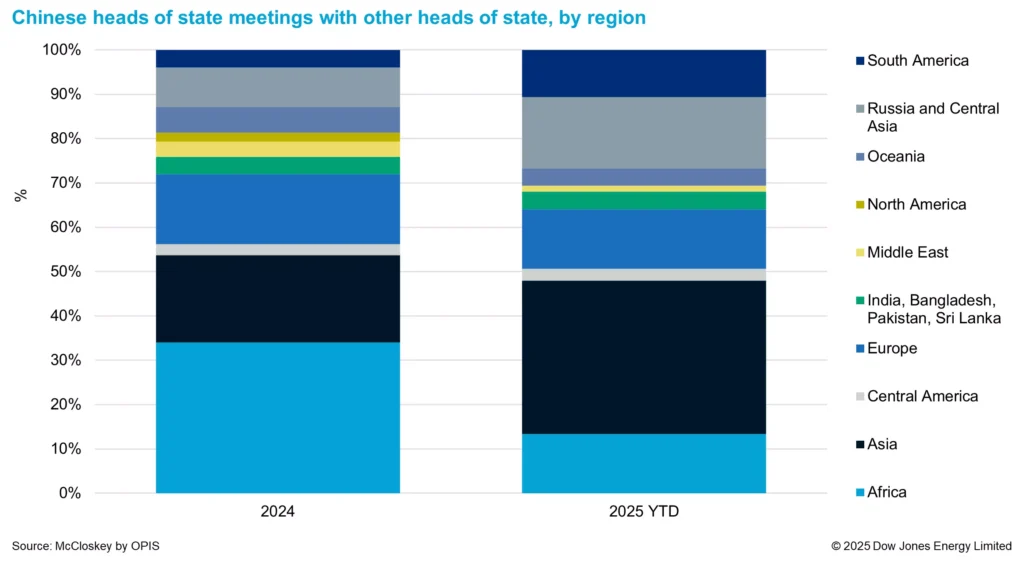

Looking at the regions of the world where these foreign leaders are from is particularly telling (Figure 1), with significant changes from 2024 to 2025.

Figure 1.

China’s belt and road initiative has had a longstanding focus on Africa, Central Asia, and in more recent with smaller island nations in Oceania. Meetings with African heads of state have plummeted (though this is significantly a function of many visits in Q3 2024 as noted above), as have meetings with those from Oceania.

Meanwhile, meetings with Asian countries – particularly those in Southeast Asia have soared. This is unsurprising given the press coverage that those meetings have gotten. But covered little in the general press is a surge in meetings with heads of South American countries (and not just BRICS-peer Brazil). Meetings with countries in Central Asia have soared too. Interesting, meetings with countries on the Indian subcontinent have shrunk, albeit slightly.

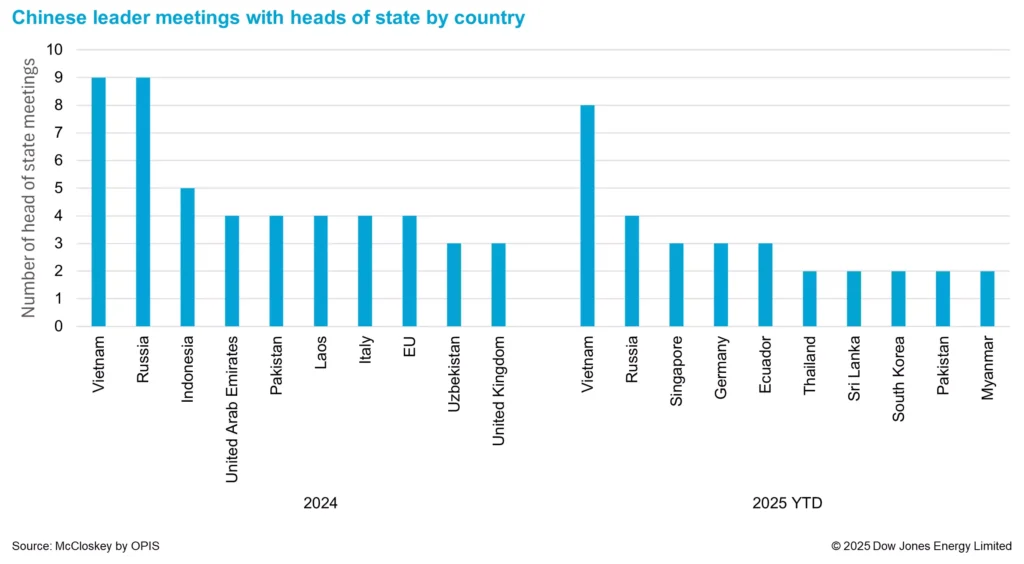

Looking at individual countries is also revealing (Figure 2). Chinese leaders met with the leaders of Vietnam and Russia (9 times each) more than any other country in 2024. And Chinese leaders have met with Vladimir Putin at roughly the same rate so far in 2025, but meetings with Vietnam’s leadership have almost hit the 2024 number just in the first 6 months of 2025. Vietnam is clearly a Chinese focus right now as it looks to offset lost trade elsewhere.

Figure 2.

Meetings with other countries in Southeast Asia – including Singapore – have also grown. Interestingly, there has only been one meeting with Indonesia’s President Prabowo Subianto, and that was held by Li Qiang, not President Xi. Indonesia had 5 meetings with China in 2024.

What does all of this mean for commodity markets?

China is refocusing, looking to replace lost trade with the US, and also to secure its own supply chains and markets amid a somewhat uncertain future.

China is obviously a huge commodity buyer and seller, and we wrote about China’s exposure to crude oil – particularly that from Iran – in an earlier Tariff Talk. But one of the most telling meetings for commodities in our view on July 15 when Australia Prime Minister Anthony Albanese visiting President Xi in Beijing, as part of a 6 day visit to China. The meeting was remarkably warm and cordial, considering the trade war between the two countries that lasted from 2020 until 28 March 2024. While there were some expressions of concern about military exercises by both countries, both sides expressed that they were happy to have moved on from the trade war.

Most tellingly, green Iron (iron produced using hydrogen produced using renewable electricity) was discussed. And alongside government officials, a delegation of Australian iron ore miners met with Chinese steel mills. The idea of green iron being produced in northern Western Australia, and being exported to China in the form of hot briquetted iron (HBI) was the focus of discussions. Green iron is expensive to produce currently, and Australia is hoping for Chinese investment to help bridge the cost gap, with the benefit of also helping both countries decarbonize. A green iron hub in Western Australia would potentially compete with the apparent development of a green iron hub in the Middle East (McCloskey research subscribers can see our Middle East Green Steel Profile and Green Steel Projects Database for more detail; non-subscribers can request more information on these services).

Even if Green Iron never really eventuates, the cordial meetings suggest that trade between Australia and China may strengthen, and that the risks of a recurrence of the China-Australia trade war have significantly diminished. This has obvious implications for the future of trade of iron ore and metallurgical coal, as well as the trade of Chinese steel to Australia – not to mention many other commodities.

Both countries have concerns about trade amid the current US administration, and concerns that similar issues may continue or might recur in the future. Practical realities dictate that diversification is important. That said, perhaps in a classic example of short memories, it is interesting to remember how a key focus by Australian producers during the China-Australia trade war was a need to diversify away from being too focused on the Chinese market. It is ironic that the current US administrations actions may be moving Australia and China closer together again, though it may end up being to the betterment of both countries. President Xi summarized the meetings by saying that the relationship had improved “from the setback and turned around, bringing tangible benefits to the Chinese and Australian peoples.”