The Octane Squeeze: How Tightening Specifications are Reshaping Fuel and Chemical Markets

Over the course of its production history, gasoline has evolved from an economically produced, high energy density fuel to an energy source that must satisfy stricter engine performance needs and meet greater regulatory hurdles. While refiners continue to produce gasoline to meet changing transportation and specification needs, there are significant ramifications to key chemical markets, such as aromatics, which greatly interface with gasoline production.

Strengthening Octane Demand

Gasoline is currently pressured from three sides. First, modern gasoline internal combustion engines (ICE) increasingly require higher-octane gasoline to achieve higher compression ratios and avoid engine knock. Second, environmental restrictions are increasing which provide greater limits on which blendstocks are viable in gasoline streams. Regulations like US EPA Tier 3, Euro VI, or China VI have pushed for more stringent emissions standards that have spurred demand for cleaner, high-octane components. These regulations also include measures to remove sulfur which destroys octane, resulting in a structural deficit that must be filled by merchant octane sources, including aromatics. Lastly, overall demand for gasoline is waning with the penetration of electric vehicles (EV) into the transportation fleet. The result has been a widening value gap between low-grade and high-grade blendstocks and a decoupling of octane values from gasoline prices, a trend that is likely to continue as overall gasoline demand begins to decrease in many parts of the world.

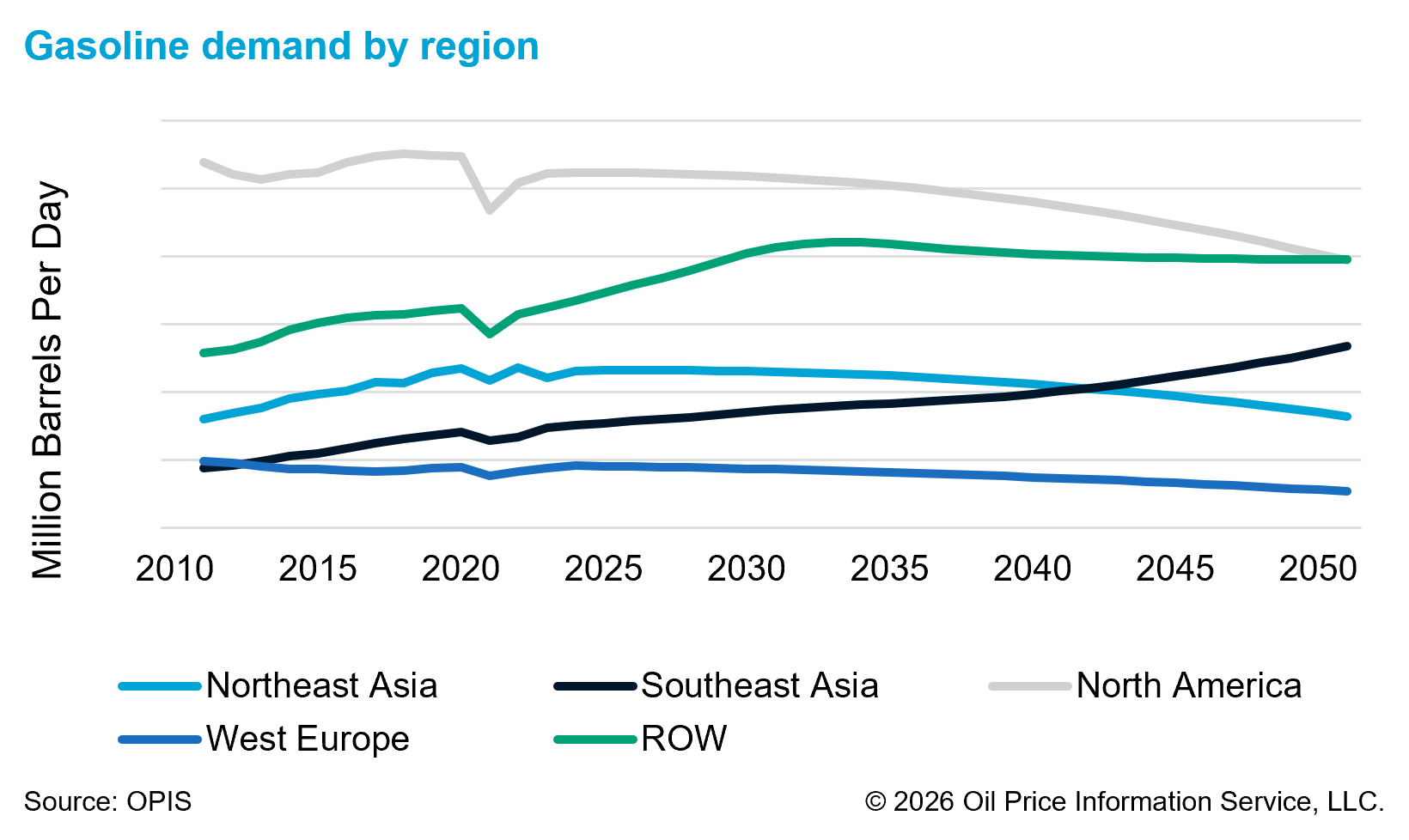

Slowing Gasoline Demand

The pace of the energy transition is changing, as political outcomes, rising trade barriers, waning enthusiasm for EVs plus the rise of artificial intelligence (AI) complicate an accelerated shift away from hydrocarbon-based fuels. The energy industry has invested an enormous amount of capital over the last century to produce, refine, and deliver hydrocarbon-based fuels and products, and this value chain is not easily replaced. While the automotive and manufacturing industries have adopted EVs and hybrids to enhance future fuel efficiency, these technologies will assume growth in mobility rather than a wholesale replacement of the existing mobility. In short, the need for octane will continue to expand and with that, gasoline demand grows, peaking in the 2030s before gradually declining in the 2040s. Ultimately, the result is a world that gradually evolves its energy mix rather than abruptly transitioning to new energy sources.

The pace of the energy transition is changing, as political outcomes, rising trade barriers, waning enthusiasm for EVs plus the rise of artificial intelligence (AI) complicate an accelerated shift away from hydrocarbon-based fuels. The energy industry has invested an enormous amount of capital over the last century to produce, refine, and deliver hydrocarbon-based fuels and products, and this value chain is not easily replaced. While the automotive and manufacturing industries have adopted EVs and hybrids to enhance future fuel efficiency, these technologies will assume growth in mobility rather than a wholesale replacement of the existing mobility. In short, the need for octane will continue to expand and with that, gasoline demand grows, peaking in the 2030s before gradually declining in the 2040s. Ultimately, the result is a world that gradually evolves its energy mix rather than abruptly transitioning to new energy sources.

Impact on Aromatics

The development in the decoupling of octane values from gasoline prices and the structural octane deficit are particularly important for toluene and mixed xylenes, which serve as staples of the gasoline blend pool due to their high octane, low RVP characteristics and limited environmental restrictions. As certain aromatics become increasingly attractive to the gasoline blend pool, chemicals and solvents players will have to be prepared to bid molecules away from the blend pool. The theoretical blend values effectively function as a price floor, sometimes pricing out solvents consumers as blend values exceed chemicals market prices.

These octane boosters are also susceptible to geopolitical forces. This has become especially apparent in the past year due to new trade wars and the start of the US/Israel conflict with Iran, which have forced market participants to become more acutely aware of octane trade flows and supply chains. Refinery rationalization in Europe and the US Northeast has the potential to make these regions octane-short, increasing their reliance on large-scale refiners in the Middle East and mainland China. Furthermore, as mainland China’s domestic gasoline demand stalls due to rapid EV penetration, its large-scale integrated refineries are pivoting away from transportation fuels to maximize chemical yields. With mainland China’s goal to achieve petrochemical self-sufficiency, its internal pull for toluene and mixed xylenes into its domestic chemical sector will continue to grow further reinforcing the high price floor for high-octane gasoline components.

Long-Term Outlook

As gasoline markets lengthen in the longer term, catalytic reformers designed to produce high-octane blendstocks (reformate) will likely pivot to lower operating levels justified primarily by chemical values over gasoline demand. Looking beyond this decade, the bio-octane sector is likely to transition from a niche interest to a more critical lever of the blend pool. However, biomass-derived aromatics will remain challenged by higher production costs and issues related to raw material collection and catalyst deactivation.

Ultimately, the octane market is entering an era defined by concentration rather than expansion. While the peak gasoline narrative suggests a sunsetting industry, the reality is a transition toward a high-complexity, high-value specialty segment. As the energy transition progresses, the octane spread will likely serve as a barometer for a refinery’s competitiveness in an increasingly carbon-conscious and supply-constrained world.

–Drew Galvin (andrew.galvin@chemicalmarketanalytics.com)