The Shifting Global Rubber Markets

Natural and synthetic rubbers are key components for global tire production. While post-COVID concerns over component supply chains have been mostly relieved, vehicle producers continue to face headwinds from U.S. import tariffs on vehicles, persistently elevated inflation and interest rates, and the recent Middle East conflict.

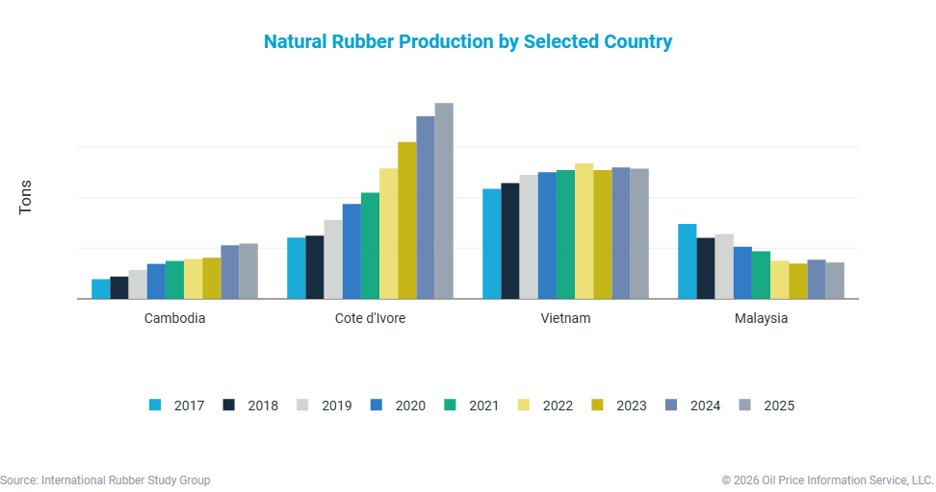

In 2025, Southeast Asia remained the key global supplier of natural rubber, though production has declined among traditional major producing countries including Thailand, Indonesia, and Malaysia due to low natural rubber prices, reduced rubber processing capacity, and tree disease. The industry is also concerned over weather-related disruptions, including heavy rains, flooding, and the potential severity of the “El Niño” drought effect. While production fell among traditional producing countries, levels continued to rise in non-traditional producing countries like Cote d’Ivoire, which has become the third-largest producing country, as well as Cambodia, Laos, and Myanmar.

However, declining total plantation area in Southeast Asia presents a concern for the long-term production outlook, as low natural rubber prices have reduced investment in existing and new plantations. While higher production can be achieved by increasing agricultural yields, this requires investment in training on farming, tapping, fertilization, pest and blight management, practices that are difficult to implement for the small holders who dominate global production. Furthermore, natural rubber trees require a growth period of 6 to 7 years before production can begin. In the longer term, the global market may face structural supply shortages if plantation area continues to decline amid gradually rising demand.

Global light vehicle production continues its slow recovery towards pre-pandemic levels, but the automotive industry faces challenges from tariffs, geopolitical risk, inflation, and interest rates which pressure global consumption. Natural rubber demand depends heavily on the automotive and tire sectors of which Asia accounts for the vast majority. Meanwhile, natural rubber demand from Europe has contracted, due primarily to sanctions on Russian tire imports.

On the feedstock side, elevated energy costs have led to increases in production costs for synthetic rubber, widening its price spread with natural rubber. As synthetic rubber prices have significantly exceeded natural rubber prices, the natural to synthetic price ratio has fallen outside its historical baseline range, leading to substitution between the two rubbers and putting pressure on the synthetic rubber value chain.

These trends in natural rubber have a significant impact on the C4 olefins value chain. There are significant concerns about medium- and longer-term market dynamics. Decreasing production from traditional key producing countries has left the industry increasingly reliant on emerging suppliers to compensate for those losses. Longer term, the supply side risk is primarily caused by poor economics in the short-term threatening reinvestment that will be required to meet future demand. Demand growth continues to face downside risks due to the current geopolitical turmoil. These supply and demand pressures, coupled with rising prices for synthetic rubber due to current tightness in energy and base chemical markets, are shaping the wider rubber value chain.

-Anthony Song, Executive Director, Olefins & Derivatives (anthony.song@chemicalmarketanalytics.com)