The Three Dimensions of Price: Inside the Global Polyester Stalemate

When a geopolitical shock upends a global supply chain, market observers typically look to crude oil benchmarks to gauge the damage. However, the ongoing closure of the Strait of Hormuz demonstrates that a structural crisis does not express itself in a single, linear price spike. Instead, prices evolve across three distinct, sequential dimensions: cost-push, supply-shock, and demand-validation. Understanding this framework explains how the physical blockage of a maritime chokepoint has transformed into a psychological standoff threatening American consumer packaging.

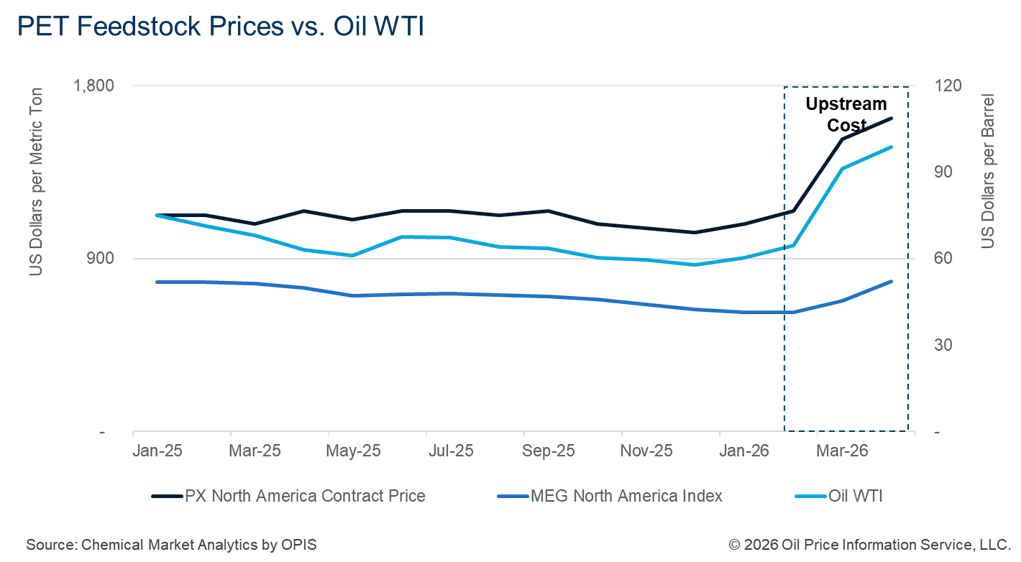

1 – The Upstream Cost-Push

The immediate reaction to the late-February closure was defined by input costs. With Middle Eastern crude, LPG and critical chemical derivatives stranded in the Persian Gulf, the raw cost to produce downstream products surged. Because Asian polyester manufacturers rely heavily on naphtha-based crackers, this energy spike instantly steepened their production cost curves, forcing a baseline increase in global prices simply to protect bleeding manufacturing margins.

2 – The Downstream Supply-Shock

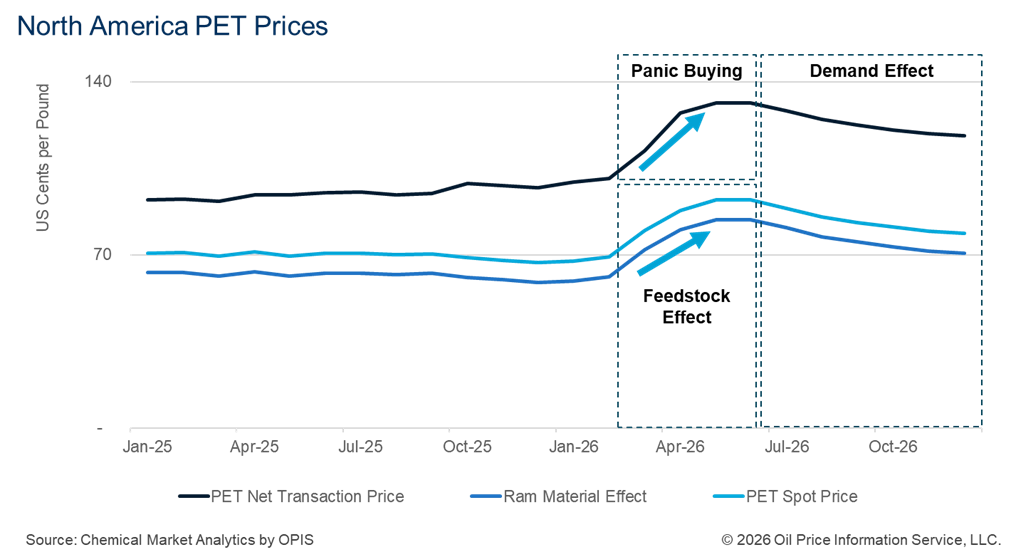

As the crisis dragged on, the second dimension took over: pure physical availability. Deprived of Middle Eastern precursors, major manufacturing hubs, like South Korea and Taiwan, were starved of raw materials, forcing widespread reductions in operational rates. Because the US relies on these Asian suppliers for roughly 20% of its import pipeline for polyethylene terephthalate (PET)—the essential plastic resin used to manufacture water, juice, and soda bottles among other products—the global export pool cratered. This triggered a wave of “panic buying.” Fearing outright structural shortages ahead of peak summer demand, consumer goods companies aggressively hoarded resin, bidding prices up to historic premiums regardless of cost.

Dimension 3: The Demand Stalemate

Today, the market has entered the third, most complex dimension: demand validation. This phase is governed entirely by behavioral psychology. While upstream costs remain high and physical supply remains tightly constrained, the pricing rally has hit a psychological ceiling. Buyers have effectively launched a strike. Plastic converters, distributors, and brand owners realize that if economic headwinds cool consumer spending, they will be left holding expensive resin inventory that the retail market cannot support. Conversely, if they buy nothing, they risk localized product shortages during the high seasonal demand of summer, amplified by the North American World Soccer Cup.

This three-dimensional evolution shows that a supply chain crisis eventually shifts from an operational emergency to a financial game of chicken. The current market stalemate has frozen procurement pipelines just as peak seasonal demand arrives. In global trade, the paralyzing fear of buying at the absolute market top can create an artificial inventory vacuum just as severe as the physical blockade itself.

As of now, the supply chain has exhausted low-cost pre-conflict inventory, and higher production costs will eventually flow through over the next couple of months to the final consumer, which should at least support plastics pricing near current levels. Longer-term there is a risk that inflation erodes consumer purchasing power and leads to demand reduction which could balance plastics markets more rapidly.

Meanwhile, the market is catching its breath and moving past panic buying that characterized the early stages of the Middle East disruption. PET buyers have generally moved to an as needed purchasing strategy with most parts of the supply chain limiting inventory risk.

– Roberto Ribeiro, Vice President Ethylene Oxide and Derivatives & PET (roberto.ribeiro@chemicalmarketanalytics.com)