Unpacking the EU Plastics Tax

Introduced as part of the 2021–27 EU budget, the EU plastics levy requires member states to contribute to the EU budget at a rate of €0.80/kg of non-recycled plastic packaging waste. Although often discussed in the context of circularity, its primary function is fiscal, as revenues are not directly earmarked for recycling infrastructure. The levy reinforces a broader policy direction, working in combination with recycled-content mandates, extended producer responsibility (EPR) schemes, and packaging design rules, to add indirect cost and compliance pressure to the polyolefins sector.

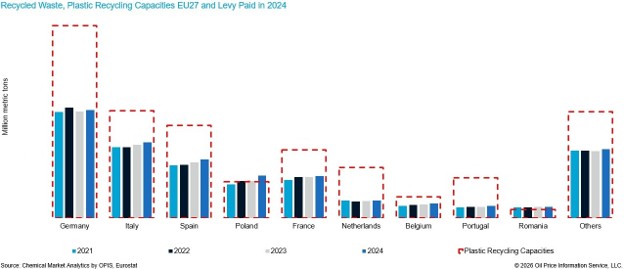

Because the EU does not prescribe a uniform domestic mechanism for recovering the levy’s cost, a fragmented policy landscape has emerged. Spain provides the clearest example of a direct domestic pass-through, introducing a special tax of €0.45/kg on non-reusable, non-recycled plastic packaging that directly influences converter material choices. On the other hand, France absorbs the budget burden through public revenues, creating a weaker immediate signal for polymer buyers. This unevenness amplifies differences in converter economics, packaging strategies, and procurement decisions across Europe.

The main constraint on Europe’s plastics recycling industry is the interaction between weak demand, variable feedstock quality, high processing costs, and low-cost virgin polymers imports. While high energy costs challenge domestic virgin polymer producers, recycling is also energy-intensive, meaning European power and gas spikes do not automatically create an open window of opportunity for recyclers. Furthermore, collection and sorting systems remain a structural weakness across member states, resulting in high contamination levels that limit the scale of recyclate supply capable of broadly displacing virgin polyolefin demand.

Another risk for the plastic recycling industry is that virgin resin remains difficult to displace in many packaging applications due to food-contact requirements, technical performance standards, and limited availability of high-quality recyclate. The realistic near-term risk is slower growth in virgin packaging demand, greater price pressure, and weaker margins where imported virgin and recycled material caps domestic price recovery.

The next phase in the policy path will be shaped less by the EU levy and more by the wider packaging and circularity framework, for example the Packaging and Packaging Waste Regulation (PPWR). The PPWR transitions the policy focus from a fiscal contribution based on non-recycled waste toward operational requirements with strict criteria regarding recyclability, recycled content, labelling, collection, and design. In a weak economic environment where broad new taxes on plastics are becoming harder to justify politically, policymakers favor these targeted instruments, which increase slow structural pressure on packaging grades.

While the EU plastics levy itself does not present a direct threat to the plastic industry, the broader circularity agenda will continue to materially alter packaging procurement patterns. If policymakers want to reduce dependence on virgin plastics while preserving industrial competitiveness, legislation must go beyond fiscal burdens to stimulate stronger end-market demand for recyclates, harmonize collection and sorting networks, improve feedstock quality, and ensure credible enforcement against non-compliant imports.

For more insights and in-depth coverage of the circular economy and plastic recycling, explore Circular Plastic Service.

– Svetlana Panteleeva, Associate Director, Plastics & Polymers (svetlana.panteleeva@chemicalmarketanalytics.com)