When Ethylene is Optional: Coal-Based Supply is Stepping Up

Amid ongoing disruptions to Middle East energy and chemical feedstock flows, the impact is extending beyond feedstocks into the petrochemical chain, with regional steam crackers operating at reduced rates or offline, significantly curtailing olefin and derivative exports.

The escalating geopolitical conflict in the Middle East has triggered a “double shock” for Asia, abruptly halting over 15 million metric tons of annual “contained ethylene” exports—primarily PE and MEG—while simultaneously choking off critical naphtha feedstocks. Unable to offset the deficit through local oil-based production, the extreme supply constraint is forcing Asian buyers to absorb exorbitant freight premiums for Western replacement cargoes.

This is reinforcing the need for mainland China to lift domestic production, not only of light olefins but also of downstream derivatives. The present situation heavily advantages China’s domestic coal-to-chemicals sector, which remains insulated from the blockade and international oil shocks, allowing it to operate at maximum rates to backfill the massive regional supply void.

In this context, coal-based value chains are gaining renewed strategic importance on two fronts. Coal-to-olefins (CTO) routes are helping to backfill domestic supply, partially offsetting reduced imports and supporting downstream integration, in particular polyolefins.

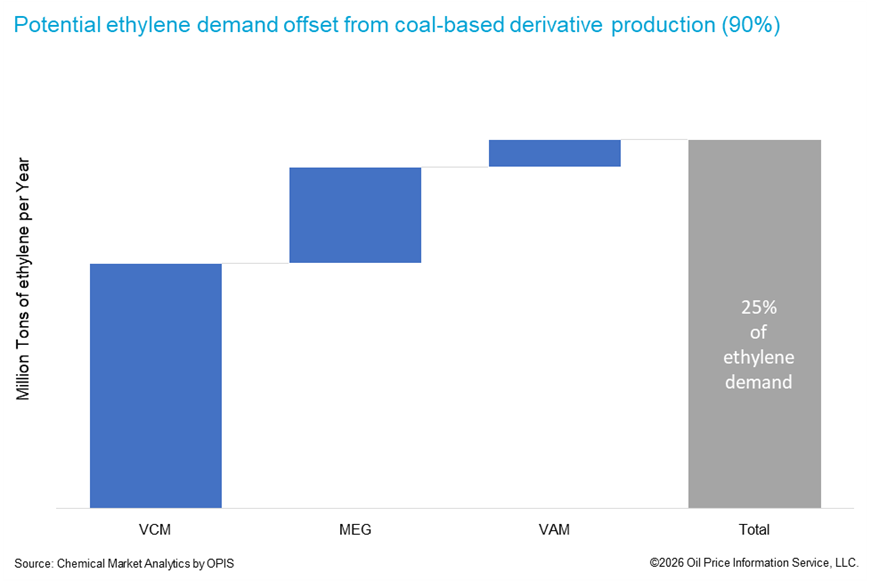

At the same time, coal-to-chemicals pathways producing polyvinyl chloride (PVC), vinyl acetate monomer (VAM) and monoethylene glycol (MEG) provide direct derivative supply without relying on conventional ethylene productions, effectively bypassing one of the most disrupted links in the value chain.

Notably, the pace of new coal-to-chemicals development had slowed in recent years. However, the ongoing crisis is driving a renewed strategic reliance on the coal-to-chemicals sector, which is rapidly ramping up operating rates.

As market tightness and logistics constraints persist, the combined role of CTO and coal-to-derivatives is enhancing supply resilience and optionality, reinforcing mainland China’s push toward greater self-sufficiency while cushioning the impact of lost Middle East exports.

Because these facilities have historically operated with significant spare capacity, increasing their aggregate utilization to 90% would allow them to support up to 25% of China’s total domestic ethylene demand, effectively deploying an additional 8% of domestic supply as a powerful, localized shock absorber.

Ultimately, this period of heightened volatility underscores the critical importance of feedstock diversification and supply chain resilience, highlighting a widening competitive divide where resource-advantaged regions can stabilize their markets while import-dependent nations remain structurally exposed.

-Reporting by William Chen, VP Asia Olefins (william.chen@chemicalmarketanalytics.com) and Mike Park, Director Asia Olefins (mike.park@chemicalmarketanalytics.com)