Engineering Resin Market Exposure to the Iran Conflict

Engineering Resin Price Impact

Shipments through the Strait of Hormuz have virtually come to a standstill, as major shipping lines have suspended transit through both the Red Sea and the Suez Canal due to severe and escalating security risks. There are no shipments departing from Iran, Eastern Saudi Arabia, Kuwait, or Qatar, and Omani ports are heavily congested. Vessels bound for the Middle East are now discharging cargo and idling at alternative ports—including locations in India, Sri Lanka, and broader Asia—because onward passage is not viable under current conditions.

Shipping costs have increased significantly. War-risk and risk-premium surcharges have risen sharply, insurance premium on shipping containers have skyrocketed adding further uncertainty to commercial operations.

Prior to the conflict escalation, some ~25% of global oil, LNG, and NGL flowed through the Strait of Hormuz. Even prior to significant infrastructure damage in the third week of the conflict, the closure of this chokepoint in the early days of the war drove significant volatility across energy, feedstock, and freight markets; Qatar’s LNG suspension intensifies global supply risk.

PC, ABS, Nylons, PBT & POM should be affected globally due to rising crude, gas, and derivative feedstocks—alongside freight costs, which have doubled from Middle East origins—pushing buyers in Europe and Asia toward US supply. Broader chemical value chains are tightening, with higher Benzene, Styrene, Phenol, Ammonia, and Propylene costs, emerging ammonia constraints in the Middle East, and elevated European gas prices sustaining upward pressure on production costs and thus affecting engineering resin prices.

Engineering Resin Global Production Impact

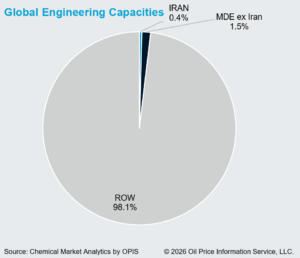

The Middle East has a global share of Engineering resin (PC, ABS, Nylon 6, Nylon 6,6, PBT & POM) capacity of about 3%. Indeed, global engineering resin production capacity remains well diversified geographically, with most output located outside the conflict-affected regions. Thus, even in the event of a complete production shutdown within the Middle East, the overall global production of engineering resins would remain largely unaffected. Notably, one significant Polycarbonate (PC) producer is in Saudi Arabia.

The geographical diversity of Engineering Resins assets means production disruption in the Middle East specifically has minimal to no effect to global Engineering Resins markets. While disruptions may temporarily affect buyers tied to Middle Eastern contract volumes, they still have readily available alternative suppliers. The diversified global producer base enables procurement shifts.

However, feedstock cost and availability could cause significant disruptions to Engineering Resins costs and potentially result in production cuts and impact supply/demand dynamics. Inevitably, feedstock costs are on the rise, and this will also play an important part in prices of Engineering resins.

Oil, gas, and petrochemical feedstocks’ price and availability, as well as mandated prioritization of fuels production over petrochemicals in some countries, will also affect global Benzene availability.

Asian crackers rely heavily on Middle Eastern naphtha. As supply has been dried up, multiple producers have cut their utilization rates or declared force majeure across South Korea, Indonesia, Mainland China, Taiwan, China, Japan and Singapore.

This feedstock disruption has created a structural shortage in the production chain for major engineering plastics, including polycarbonate (PC) and acrylonitrile-butadiene-styrene (ABS). With upstream costs rising due to surging crude and naphtha prices and reduced cracker output, producers are facing significantly higher raw-material costs, directly impacting the cost structure of PC and ABS across the region. Asian buyers across India, Bangladesh, Thailand, and Vietnam are struggling to secure prompt cargoes, with several tenders going unawarded due to insufficient supply.

—Reporting provided by Paula Sans Quiros, Executive Director Engineering Plastics