The Impact of US-Iran Conflict on Methanol Markets

Supply

Iran occupies a structurally significant position in the global petrochemical value chain, particularly in methanol, boasting 11% of global methanol nameplate capacity making it the world’s second-largest methanol producer, after mainland China. Iran exports well over 90% of its methanol production to the global markets mainly to mainland China and India.

Given methanol’s role as a fundamental feedstock for methanol to olefins (MTO), formaldehyde, acetic acid, MTBE, direct fuel and various downstream applications, the ripple effects of a sustained Strait of Hormuz blockade would extend well beyond the primary methanol market.

Iran is the principal source of imported methanol in Asia, especially to mainland China’s east coast. Its export-oriented production model means that any logistical or geopolitical constraint directly translates into reduced global spot and contract volumes.

Power outages have reduced Iranian operating rates to below 60% in some areas, increasing shutdown risks. At the time of writing, no confirmed production disruptions have been reported in Saudi Arabia, Kuwait, Oman or the UAE, although operators remain cautious amid heightened security risks, energy infrastructure being targeted across the region, and rising inventories.

Trade

Due to Iran’s unique geopolitical position and the ongoing trade sanctions, there is no official data on mainland China’s methanol imports from Iran. However, estimates suggest that at least 50% of mainland China’s imported methanol originates from Iran. The primary end-users are private MTO producers located on mainland China’s coastal areas, where methanol serves as a critical feedstock to produce olefins and various olefins’ derivatives.

{kind=link}

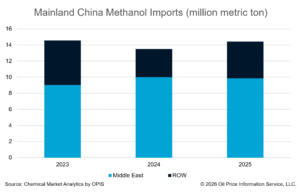

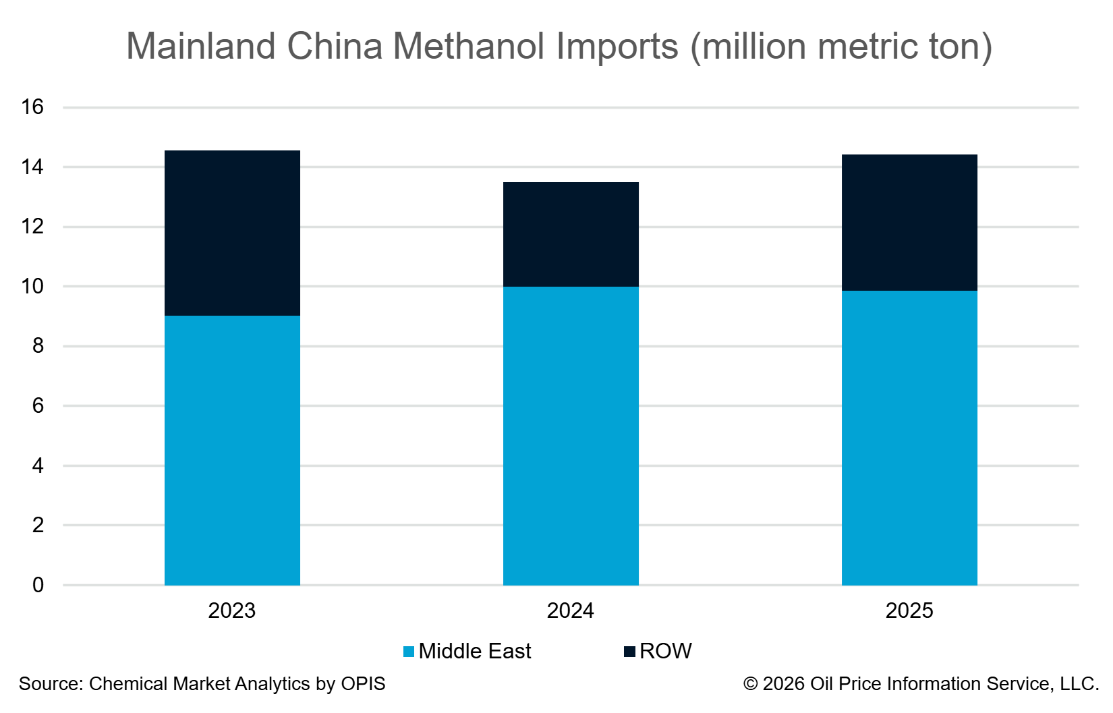

The current conflict, however, does not only impact Iran; it has broader implications for the entire Middle Eastern petrochemical supply chain. Methanol sourced from the Middle East accounts for approximately 70% of mainland China’s total imports, highlighting the region’s importance to Chinese supply security. Beyond mainland China, Middle Eastern methanol also represents a key import source for other major Asian markets, underscoring the systemic nature of supply risk in the region. Western Europe receives no direct methanol supply from Iran due to the international sanctions. Suppliers from Saudi Arabia and Oman hold a relatively small share of the European spot and contract markets, but they play an important role in providing spot liquidity and balancing supply.

Prices and m. China’s MTO economics

Following the escalation of the conflict, China’s methanol futures experienced a sharp surge on 2 March, hitting the daily price limit before the afternoon close. In the physical market, methanol spot prices in East China rose by more than RMB 100 per metric ton compared with the previous Friday. The MTO sector already operates with low or even negative cash production margins under normal economic conditions. It is now likely to face additional short-term pressure, elevated methanol prices, potential supply uncertainty, increased feedstock and utility costs and reduced operational flexibility.

For marginal or high-cost MTO plants, this is likely to result in temporary cutbacks or lower operating rates. However, rising production costs are not limited to the MTO sector, as other olefin production routes are also facing significant pressure. The closure of the Strait of Hormuz has severely disrupted global trade flows of key olefins feedstocks, including methanol, crude oil, naphtha, and ethane, causing feedstock prices to rise sharply. Given their heavy reliance on imported feedstocks, domestic oil-based olefins producers have responded lowered operating rates by varying degrees. Tight crude supply and surging feedstock prices have reshuffled the relative costs of the different olefin production processes. As the market continues to evolve and the duration of geopolitical disruptions remains uncertain, the MTO economics and operating rates should remain dynamic.

Outlook

The Strait of Hormuz is closed, driving higher transportation costs and insurance premiums while inventories are building rapidly across the Middle East region. Production limitations are therefore expected to emerge not only in Iran but potentially also in Saudi Arabia and Qatar. Overall, these developments are likely to support higher global methanol prices, broadly tracking movements in crude oil.

However, the sustainability of this price spike, as well as the availability of Iranian methanol supply, will depend largely on the duration of the conflict and potential changes in Iran’s political and regulatory landscape.

—Reporting by Mike Nash, Vice President Syngas; Xiaomeng Ma, Director Asia Methanol; Andrei Akhzigitov, Director EMEA Methanol; Maia Dolan, Director Americas Methanol